Gas industry of China

Resume

China is the second largest gas market in the world and the world's largest importer of LNG. In the ranking of importers, China replaced Japan in the first place.

In 2025, China became the fourth-largest gas producer in the world.

In 2025, Qatar became the largest supplier of LNG to China (20.4 million tons). Australia dropped to second place (20.3 million tons) due to anti-Chinese intrigues. Russia has risen to the third place (7.5 million tons). If we take into account pipeline supplies, Russia is the leading supplier of gas to China. Malaysia is the fourth-largest importer of LNG (7.1 million tons). Indonesia is the fifth-largest importer (4.1 million tons).

China is at the center of US political intrigues in the global LNG market. China imports LNG from Russia, including those that are blacklisted by the West. Additionally, due to the Trump trade war, China has stopped importing US LNG and is reducing its imports of Australian LNG due to anti-China military alliances.

China is the leader in small-scale LNG production, with hundreds of plants with a combined capacity of over 50 million tons of LNG per year.

China is the second largest shipbuilder of LNG carriers after South Korea right now. Its share in the portfolio of gas carriers under construction is continuously growing and currently stands at 27%.

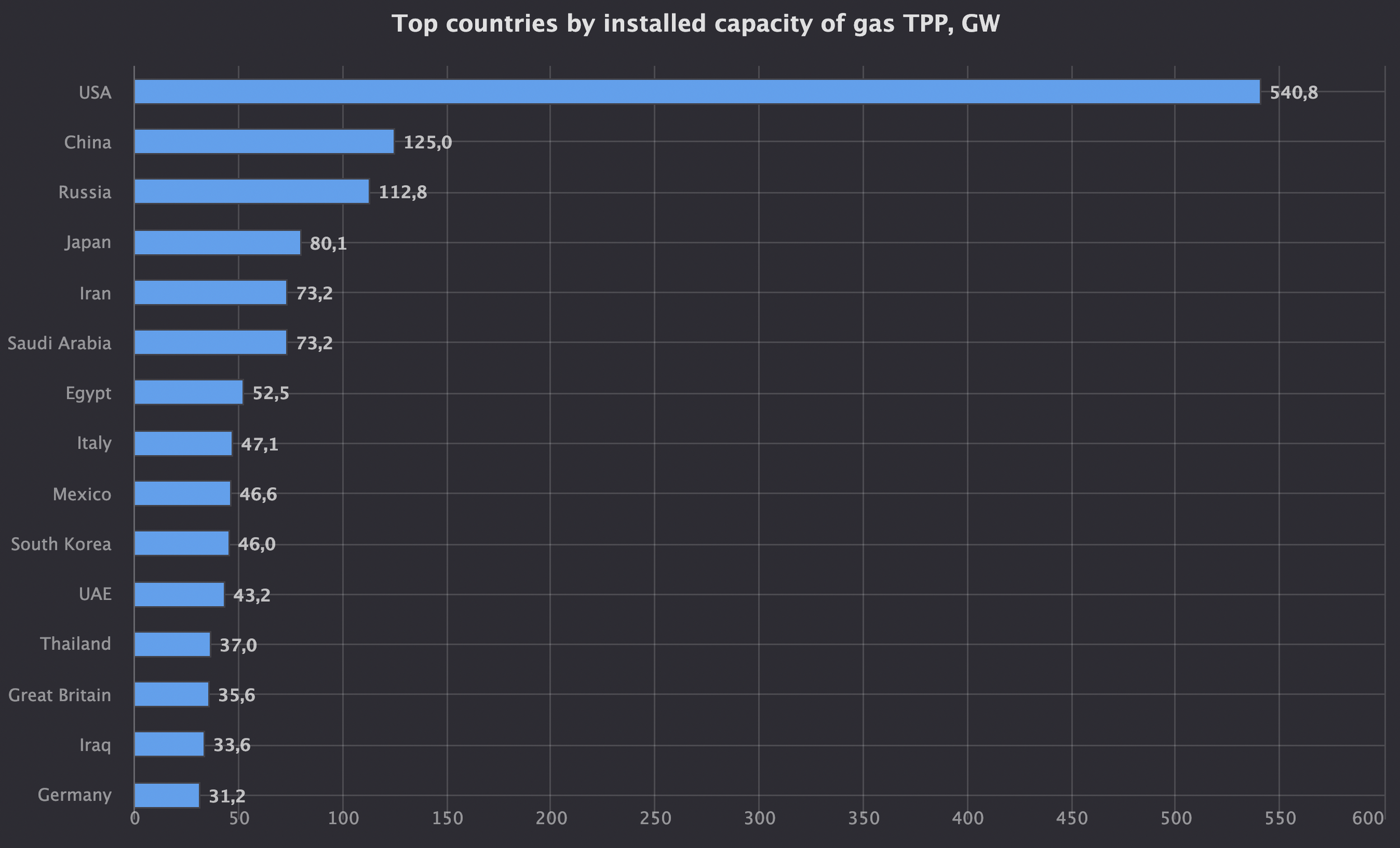

China is the second-ranked in the world by installed capacity of gas-fired TPPs.

Map of gas industry

Chinese natural gas market

Demand

Domestic demand for natural gas is growing rapidly.

China is actively developing the use of LNG as fuel for heavy trucks.

Gas-fired power generation

Сoal still dominates China's energy and heat supply. Natural gas, along with renewable energy sources and nuclear energy, are types of energy that should not only cover the rapid growth of China's demand for energy, but also reduce the share of thermal coal in the energy mix.

China is the second-ranked in the world by installed capacity of gas-fired TPPs. Installed capacity of gas-fired TPPs in the country is 125 GW. Theoretical maximum demand from gas generation is 753 mcm/d.

Production

China's domestic gas production in 2023 amounted to 230 bcm. Annual increase is 10 bcm.

In 2025, China became the fourth-largest gas producer in the world.

China is actively developing extraction of unconventional gas reserves, including coal methane and shale gas.

In 2025, 276 million tons of coal were gasified to produce methane and motor fuel. Estimated methane output is around 55 billion cubic meters, equivalent to a quarter of domestic natural gas production.

Shortage of domestic gas is covered by pipeline supplies from neighboring countries and LNG import.

Pipeline import

China imports pipeline gas from Russia (Power of Siberia and transit through Kazakhstan), Central Asia (Uzbekistan, Kazakhstan, Turkmenistan) and Southeast Asia (Myanmar).

Russia

In 2025, Russian gas accounted for 27% of China's pipeline gas imports.

Power of Siberia is the main export route of Russian pipeline gas to China.

Supply by year:

2023 - 30.0 bcm.

2024 - 31.1 bcm.

2023 - 38.8 bcm. Exceed of the contract volume by 800 mcm.

In September 2025, agreement was reached to increase the supply through Power of Siberia-1 from 38 to 44 bcm per year.

Price formula in the contract is linked to crude oil price indexes and averaged over 9 months. This type of formula price was typical for long-term contracts for pipeline gas and LNG at time of contract signing, but the multiplier coefficient to oil index (“slope”) is lower than the industry standard of 12.5%. This indicates that Russia provided to China a discount.

Since 2015, Russia and China have been negotiating construction of Power of Siberia 2 gas pipeline, which will have capacity of 50 billion cubic meters per year. The pipeline is intended to connect the existing gas fields of Bovanenkovo and Kharasavey in Yamal with China through Mongolia. For Russia, this pipeline is an option for the gasification of Eastern Siberia and, since 2019, an alternative source of supply for Yamal gas after the gradual closure of the EU market. However, the parties have not reached an agreement on the commercial terms of the supply, including the price formula and guaranteed volume.

Discussions on the technical design of the gas pipeline began in 2020 and have not progressed significantly. In 2025, Russia and China entered into preliminary agreements for the supply of pipeline gas through the Power of Siberia-2 gas pipeline. In the fourth quarter of 2025, the organization of technical design for Power of Siberia-2 began. The pipeline was included in China's 15th Five-Year Plan for 2026-2030, but without any binding provisions.

The summit of Vladimir Putin and Xi Jinping on 19-20.05.2026 did not lead to the signing of a solid contract and the promotion of the implementation of this project.

As of May 2026, positions of the parties on the contract are estimated to be as follows:

Gazprom: a long-term contract for 25-30 years with a guaranteed volume for the entire supplied volume (take-or-pay condition) with a minimum price threshold, as well as China's participation in financing capital expenditures for construction of Russian section of the gas pipeline. An important aspect is expected price level based on a pricing formula, which is considered comfortable at a level starting from $250-300 per thousand cubic meters of gas at the border.

China National Petroleum Corporation: avoidance of guarantees for purchasing the entire volume of gas and an estimated price level under the contract at a lower level ($250 per thousand cubic meters of gas at the border and below.

Far Eastern Route gas pipeline project is under construction. This export gas pipeline is an extension of existing Sakhalin-Khabarovsk-Vladivostok gas pipeline. Export section of overall system will have capacity of 12 billion cubic meters per year. The pipeline is expected to be launched in early 2027.

Turkmenistan

Сapacity of gas pipeline from Turkmenistan to China is 50 billion cubic meters per year (Central Asia - China gas pipeline system).

Сapacity of the pipeline is planned to be increased by 15 billion cubic meters per year (up to 65) in combination with an increase in production at Galkynysh gas field (up to 200 billion cubic meters per year).

Pipeline gas supplies from Central Asian countries have been limited in recent years during the winter heating period in these countries. The growth of the population and economy in these countries has led to the fact that domestic demand takes away all production in the winter months, leaving no gas for export to China. A gas union between Russia and Central Asian countries is currently being discussed, which could benefit all three countries:

Russia - additional volumes of gas exports from the fields of the European part (direct compensation for the decline in gas exports to Europe).

Central Asian countries - revenue from gas transit through existing gas pipelines (consider direct revenues to the budget with low operating costs to receive them), as well as the ability to cover deficits during peak periods of domestic gas demand (freezes).

China is an additional source of gas.

Small scale LNG production

China is the leader in small-scale LNG production, with hundreds of plants with a combined capacity of over 50 million tons of LNG per year.

Regasification terminals

China is rapidly catching up with Japan and South Korea in terms of regasification capacity. There are currently 40 terminals in China with a total capacity of 133 million tons of LNG per year.

China continues to dominate the regasification infrastructure being introduced. China continues to rely on its gas infrastructure. China is flexible in LNG purchases and does not critically depend on it — balancing is carried out by pipeline gas, coal, and hydroelectric power plants. Currently, there are 33 operating regasification terminals in China with a total capacity of 130 million tons of LNG per year.

2023 was a record-breaking year in terms of the number of regasification terminals that were commissioned - 30.7 MTPA. In 2026, an even larger new regas capacity is expected to be commissioned - 37.6 MTPA. However, many of these projects have been delayed and may not be completed.

Chinese regas capacity market is saturated. Currently, only regas projects for local gas flow optimization are pursued. There is no need for mass construction across the country.

An example of such optimization is dedication of regasification terminals for receiving blacklisted Russian LNG (Arctic LNG 2, Gazprom LNG Portovaya).

LNG imports

Structure of LNG discharges in China

Guangdong

Guangdong Province is one of the key countries in terms of LNG consumption. This is influenced by the developed industrial sector, high gas generation (50 GW of installed capacity of gas-fired thermal power plants) and the relative distance from imported pipeline gas.

The US trade war against China is introducing strong volatility in energy consumption and, as a result, LNG imports to this province.

The structure of electricity generation in Guangdong Province is significantly influenced by the generation of hydroelectric power plants.

The volume of imports is also affected by the change in the tariff grid for electricity generated by the province's gas-fired thermal power plants in 2025.

Shandong

PipeChina LNG terminal in Longkou is going to be commissioned during Summer 2026. Capacity of the first stage of the terminal will be 5 MTPA. This terminal will be expected to become the second entry point for blacklisted Russian LNG. Thus, this gas terminal follows the market strategy of Shandong oil terminals, which are specifically focuses at import of crude oil from countries blacklisted by the West (Iran, Russia, and previously Venezuela).

Taiwan

The volume of LNG imports to Taiwan Province is strongly influenced by the volume of generation of Taiwanese nuclear power plants. Reducing their output increases the demand for LNG and thermal coal from thermal power plants.

Structure of LNG suppliers to China

Australia is the largest supplier of LNG to mainland China in the last 12 months as of 01.08.2025 - 23.5 million tons.

Qatar is number two with an indicator of 16.2 million tons.

Malaysia is number three, with 6.5 million tons.

Russia

In 2025, Russian gas accounted for 21% of China's LNG imports.

Russia also supplies significant volumes of gas through the Power of Siberia main gas pipeline. Thus, Russia is the leading supplier of gas, if all transportation methods are taken into account.

LNG re-export

Chinese companies re-export some of recieved LNG for commercial reasons.

In Q1, China re-exported 1.3 million tons of LNG (19 cargoes). Of these, ten shipments went to South Korea, five to Thailand, and the rest to Japan, India, and Philippines.

Potential trade war between China and Australia

LNG imports from Australia, the largest supplier to China, were currently interrupted in 2021-2022 due to the Australia-China trade war. There was a similar suspension for purchases of other Australian goods, including coal. In 2024, Australia became a key supplier of LNG to China - 23 million tons, with a market share of 35%.

At the same time, Australia is one of the key participants in the US anti-Chinese military alliances in Asia, including:

AUKUS (USA, UK, Australia),

Quad (USA, Australia, India, Japan),

Five eyes (USA, UK, Canada, Australia, New Zealand).

ANZUS (USA, Australia, New Zealand),

Australia's bilateral treaty with Papua New Guinea.

The numerous military alliances against China and the intensification of Australia's cooperation with other countries within the framework of these alliances make the risk of a repeat of the Australia-China trade war and the suspension of all Australian LNG exports to China extremely high. The most likely replacement LNG resource for China will be all Russian LNG projects.

The Second US-China Trade War

Background

LNG imports from the United States are a direct consequence of the US-China trade war in 2019-2020. The United States has forced China to reduce its bilateral trade monetary deficit by purchasing LNG and petroleum products from the United States.

In early January 2025, the United States launched a preliminary attack on China's LNG industry, including the China Ocean Shipping Corporation, the China National Offshore Petroleum Corporation, and the Chinese state-owned Shipbuilding Corporation. This attack will mark the expected start of a new US trade war against China in the LNG industry in an attempt to save from an imminent default on government debt (3.6 quadrillion rubles as of 01/08/2025).

Pressure on Chinese companies operating in the LNG industry

China Ocean Shipping Corporation is the world's leading shipping company. Its fleet of LNG gas carriers includes 45 operating gas carriers and 40 gas carriers under construction. The total capacity of the company's current and prospective fleet of gas carriers is 6.5 million tons of LNG. This corresponds to the volume of gas carriers commissioned worldwide this year and is equivalent to 12% of the current fleet of gas carriers in the world. In 2024, the gas carriers of the China Ocean Shipping Corporation serviced LNG shipments for Petro China, China Petrochemical Corporation, China YEnEn Energy Assets, and Katarenergy..

It is the Chinese National Offshore Oil Corporation that imports half of all LNG imports to China. It owns 6 regasification terminals in China with a total transshipment capacity of 32 million tons of LNG per year. The China National Offshore Petroleum Corporation has two existing contracts with Venture Global LNG, an LNG producer from the United States, with a total volume of 2.5 million tons per year.

Chinese shipbuilders are key suppliers of LNG carriers to the global market, with a current share of about 60% of gas carriers under construction and ordered. The Chinese state-owned Shipbuilding Corporation, including its subsidiary Hudong-Zhonghua, is the largest shipbuilder of LNG gas carriers right now.

Mutual duties on goods

On February 4, 2025, China introduced countermeasures against imports of LNG and other goods from the United States as part of a mirror response to tariffs imposed by the new Trump administration on all Chinese exports to the United States. The tariff on LNG imports from the United States to China will be 15%. The volume of shipments for the last 365 days as of 02/04/2025 amounted to 3.8 million tons. This volume is not critical for either side.

Obviously, the tariff will stop LNG shipments from the United States to China and lead to a mutual redirection of flows, at least spot supplies. At the moment, long-term contracts for the supply of LNG are in force.:

Venture Global Calcasieu Pass LNG with the Chinese Petrochemical Corporation for 1 million tons per year.

Venture Global Calcasieu Pass LNG Company with China National Offshore Oil Corporation for 500 thousand tons per year.

The company "Energy of Chenier” with the Gas company “YEnEn" for 900 thousand tons per year.

The company "Energy of Shenyor" with the Chinese National Petroleum Corporation for 900 thousand tons per year.

Despite the high LNG prices, there is an opportunity on the market right now to start LNG supplies from Arctic LNG-2 in excess of LNG supplies from the United States, if there is the appropriate political will of the Chinese supreme leadership.

In early May 2025, the United States and China agreed to reduce mutual duties to 10%.

In early April 2025, after the Trump administration imposed new tariffs on almost all countries, the Ministry of Economic Affairs of Taiwan Province of China contacted the Trump Administration with a proposal to increase LNG purchases from the United States by two to three times in an attempt to reduce or eliminate the tariffs imposed. In 2024, Taiwan imported 2 million tons of LNG from the United States, which accounted for 10% of Taiwan's LNG purchase portfolio.

Mutual port charges

In the first quarter, the United States imposed an additional duty on the port entry of LNG gas carriers and other vessels built in China and/or flying the Chinese flag. In April, the approach to collecting this duty on LNG carriers and a number of other vessels was changed. The key change concerning the LNG industry is that the duty on LNG carriers associated with China will be effective only from 10/14/2028.

The potential amount of the duty deferred until 2028 is estimated at 140 US dollars (the amount of duty since April 2028) per net ton of LNG tanker built in China. The fee limit is for more than 5 port calls per year for each vessel. This is equivalent to 375 million rubles for the port entry of a standard gas carrier with a lifting capacity of 73 thousand tons.

Starting in 2028, this amount will be applied to both Chinese carriers and carriers from other countries. Presumably, there will be some exceptions for LNG carriers flying the flag of the United States or owned by companies from the United States. In addition, it is reported that companies may receive a refund of duties in the future if they order LNG tankers from US shipyards. As of 2025, the United States does not produce LNG carriers.

In addition, starting from 04/17/2029, the share of LNG exports from the United States that must be exported on gas carriers built in the United States, flying the U.S. flag and operated by U.S. companies, will gradually increase from 1% in the first two years to 15% by April 2047. These restrictions will gradually increase over the course of 22 years.

5% of the current fleet of LNG carriers was built in China. This will have an even greater impact on the construction of future gas carriers - about 25% of the gas carriers currently under construction will be built in China.

As of 07/01/2025, 42 gas carriers are flying the flags of China, including 35 gas carriers flying the flag of Hong Kong.

In October 2025, China imposed retaliatory additional port charges on ships owned by both U.S. individuals and operated by organizations where U.S. citizens directly or indirectly own at least 25% of the shares. This measure applies to both United States-flagged carriers and ships built in that country. These port charges began to be collected starting from 10/14/2025.Fees will initially be charged at a rate of 400 yuan (4.5 thousand rubles) per net registered ton. This is equivalent to 152 million rubles for the port entry of a standard gas carrier with a lifting capacity of 73 thousand tons. However, from April 17, 2026, the fee will be increased to 640 yuan (7.3 thousand rubles), and from April 17, 2027 - to 880 yuan (10.0 thousand rubles), and to 1,120 yuan (12.7 thousand rubles) from April 17, 2028.

The consequences for the gas carrier market depend on the overall outcome of the US-Russia and US-China confrontations and the effectiveness of Russia-China cooperation. It is difficult to predict these consequences, but we will try in the form of extreme scenarios.:

Scenario of “Splitting the LNG trade into parts“. In this scenario, China, losing the US market for the direct supply of its products of a wide range, integrates more with friendly and neutral countries (USA, Africa, Latin America). In terms of LNG, this means China abandoning LNG supplies from the United States and refocusing on LNG supplies from Russia while maximizing pipeline gas flows from Central Asia and Myanmar. In this case, Russian gas companies find both a sales market and solve all problems with the payment and maintenance of the fleet of gas carriers. Technologically and commercially, there are all the conditions for this right now. The United States is increasing LNG supplies to the EU, Japan, South Korea and the UK.

Scenario “US victory in the trade war". In this scenario, China increases LNG imports from the United States, similar to the results of Trump's first trade war against China. LNG imports from Russia are likely to decrease, as well as the provision of technical services and equipment supplies by Chinese companies to Russian contractors in the LNG industry. The LNG market remains unified, but without Russia's participation in it.

Shipbuilding

China is the second largest shipbuilder of LNG carriers after South Korea right now. Its share in the portfolio of gas carriers under construction is continuously growing and as of 10.02.2026 stands at 27%.

Notes:

Join Seala AI’s Linkedin page to be informed for all new future releases with new dashboards and insights.

Non-mainstream oil and gas news and views are available in Seala AI’s telegram channel.

Full set of reports for each country and much more information are available via Seala AI terminal.