Oil industry of Russia

Summary

Russia holds one of the largest oil reserves in the world. Russian oil reserves are estimated at 31.5 billion tons of crude oil and 3.7 billion tons of gas condensate as of 30.06.2025. Significant share of these reserves is hard-to-recover. As of 2024, share of hard-to-recover reserves was estimated at 52%, crude oil production from hard-to-recover reserves amounted to 32%.

Russia is Top 3 oil producing countries in the world, along with Saudi Arabia and USA. In 2024 liquid hydrocarbon production in Russian Federation amounted to 516 million tons.

Russian stated-owned Transneft is the leading oil pipeline company in the world.

USA, Ukraine, UK and EU are actively attacking Russian oil industry, including military and trade attacks.

After 2022, Russian and Russian-related companies formed one of the world's largest tanker fleet. Every fourth tanker of the most popular Aframax class is controlled by Russian-related companies. Related economic sectors are actively developing, including alternative payment channels for hydrocarbon supplies, marine insurance and reinsurance, technical management of vessels.

Russia is one of the world's largest exporters of crude oil and refined products. As of 2025, the largest recipients of Russian oil are China, India, and Türkiye, while the largest recipients of fuel oil are Middle East and China, of diesel fuel - Brazil, of naphtha - Chinese province of Taiwan.

Russian oil refining industry is one of the largest in the world. Primary oil refining in Russia amounted to 267 million tons in 2024.

In recent years, there have been summer motor fuel crises due to some restrictions on availability of motor gasoline and summer spec diesel fuel. From March to November, the industry operates in a micro-management mode. Export of Russian gasoline and, to a lesser extent, diesel fuel is restricted. Belarusian gasoline is supplied to the central and northwestern regions of Russia to meet high seasonal demand.

Map of oil industry

Reserves

Russian oil reserves are estimated at 31.5 billion tons of crude oil and 3.7 billion tons of gas condensate as of 30.06.2025.

Significant share of these reserves is hard-to-recover. As of 2024, share of hard-to-recover reserves was estimated at 52%, crude oil production from hard-to-recover reserves amounted to 32%. It is predicted that in 2030, the share of oil production from hard-to-recover reserves will reach 80%.

As of 2026, share of oil low-permeability reservoir in overall reserves is 33%.

As of 2026, share of oil with high (over 80%) current water cut in reserves is 18%.

As of 2026, share of super-viscous oil (with a high content of asphaltenes, resins, and paraffins) in reserves is 4%.

Even maintaining current level of oil production in Russia requires active development of modern oil services and oil engineering, as well as active efforts to cost optimization. Economic attractiveness of oil exports will gradually decrease. It means that cheap oil from Russian is ending.

In 2024, recoverable reserves of crude oil and gas condensate of industrial categories (AB1C1) increased by 516 million tons thanks to geological exploration activities. Production amounted to the same 516 million tons. Thus, net reserves did not change.

In 2025, growth in recoverable reserves of crude oil and gas condensate of industrial categories (AB1C1) thanks to geological exploration amounted to 510 million tons. List of discovered major oil fields includes Yerkutayakhskoye oil field (11.6 million tons) and Ust-Biryukskoye gas condensate field. Volume of geological exploration works decreased in 2025: 2D seismic exploration amounted to 4 thousand square kilometers (against 5 thousand square kilometers in 2024), 3D - 16 thousand square kilometers (24 thousand square kilometers in 2024), exploratory drilling - 684 thousand meters (731 thousand meters in 2024), prospect drilling - 253 thousand meters (352 thousand meters in 2024).

Crude Oil and Gas Condensate Production

Production volumes

Russia is Top 3 oil producing countries in the world, along with Saudi Arabia and USA.

In 2023 liquid hydrocarbon production in Russia amounted to 539 million tons (1476 ktd), including:

crude oil - 476 million tons(1.3 million tons per day),

gas condensate - 46 million tons (126 ktd),

NGL - 17 million tons (47 ktd).

In 2024 liquid hydrocarbon production in Russian Federation amounted to 516 million tons (1410 ktd).

In 2024 liquid hydrocarbon production in Russian Federation amounted to 512 million tons (1403 ktd).

Share of oil produced by conventional methods was only 15% of overall liquids production in 2025. It continues to decline rapidly.

Share of new centers of oil production commissioned after 2005 was 15% in 2025.

In 2025, share of oil production from depleted fields and hard-to-recover reserves accounted 60%, including the following categories.

Oil production from low-permeability reservoirs is growing. In 2015, it was 70 million tons, and in 2025, it will reach 100 million tons. In 2025, this type of oil accounted for 19% of overall oil production. One of the factors contributing to the growth of oil production from low-permeability reservoirs is provision of tax incentives since 2013.

Oil production from reservoirs with high water cut is growing. In 2015, it was 101 million tons, and in 2025, it was 162 million tons. In 2025, this type of oil accounted for 31% of overall production. One of the factors contributing to the increase in oil production from highly water-flooded reservoirs is the transition from mineral extraction tax (NDPI) to Additional income tax (NDD) since 2019.

Production of super-viscous oil is growing. In 2015, it was 6 million tons, in 2025 - 15. One of the factors contributing to the growth of super-viscous oil production is provision of tax incentives since 2008.

Oil-producing Companies

The largest oil-producing companies:

Rosneft, including Bashneft

Lukoil

Gazprom, including Gazpromneft

Tatneft

Surugtneftegaz

Irkutsk Oil Company

Production centers

The main oil-producing regions in Russia are:

Volga-Ural region

Ciscaucasia

Timan-Pechora region

Barents Sea shelf

Western Siberia

Eastern Siberia

Sea of Okhotsk shelf

Baku fields

Baku is the first oil-producing region in Russia. Branobel (Nobel Brothers Oil Production Partnershipc) was founded in 1879 and operated oil fields in Baku, Grozny, and Chelekene. It was the first Russian vertically integrated oil company.

Nobel family's fortune, which is foundation of Nobel Prize, was earned through their involvement in Baku oil fields.

Samotlor

Super-giant Samotlorskoye oil field in Khanty-Mansi Autonomous Okrug, discovered on 29.05.1965, became foundation of oil production in Russia during late Soviet era. In Khanty language, "Samotlorskoye" means "trap lake" or "dead lake."

Its oil reserves amounted to 7.1 billion tons, which allowed it to become one of Top 10 in the world. Production began on 28.02.1969. Peak production was reached in 1983 - 215 million tons (589 ktd). In 1997, production dropped to 13 million tons (36 ktd). In 2025, production volume was about 19.5 million tons per year (53 ktd), which makes it the fourth-largest production field in Russia. Total production volume is almost 3 billion tons and 400 billion cubic meters of gas by 2025.

The field is developed by Samotlorneftegaz JSC, which is part of Rosneft group.

More than 20 thousand wells have been drilled during its development, and over 6 thousands of them are still operational. Length of the field’s oil pipelines is 1 923 kilometers and length of roads is almost 6 000 kilometers. Cities of Megion and Nizhnevartovsk were built for oil workers working at Samotlor.

Sakhalin-1

Sakhalin-1 is one of the largest oil and gas projects on the Russian shelf. It includes four offshore fields located on shelf of Sakhalin in Sea of Okhotsk.

Sakhalin-1 has one of the deepest oil wells. The deepest of them has a depth of 15 000 meters (the second deepest in the world).

Oil grade produced at the project is Sokol.

After ExxonMobil’s sabotage in 2022 the project renewed its shareholder structure. As of now it owned by Sakhalin-1 LLC. Rosneft is holder of 30% shares . The remaining shares could be claimed by Indian Oil and Gas Corporation (20%) and Japanese SODEXO (30%). ExxonMobil of USA no longer claims a share, but wants to receive “compensation”.

In the summer of 2025, a decree was signed that allowed foreign shareholders to return their shares, provided that certain requirements were met, including support for lifting of “sanctions” and transfer of funds from the project’s liquidation fund to new account at a Russian bank.

In 2025, ExxonMobil CEO Darren Woods stated that the company would not return to Sakhalin-1 project or other assets in Russia. ExxonMobil's share in Sakhalin-1 and accumulated dividends are held as collateral for future legal cases related to ExxonMobil's sabotage of the project in 2022, the US seizure of the project's liquidation fund funds in foreign banks, and the seizure of assets of Russian government and private funds in USA. As of September 2025, the value of the collateral is estimated at 382 billion rubles.

In December 2025, there were news about resumption of ONGC participation in the project. The company found a way to make the necessary payment to share capital of new Russian operator of the project. Due to Western “sanctions”, Indian companies, including ONGC, were unable to withdraw its earnings in the amount of about 66 billion rubles (3.0 bEAD / 5.7 bCNY / 76 bINR). The frozen dividends will be used to provide a loan to the Indian company, which will be used to make a mandatory contribution to a special fund for the future conservation of the field. As of August 2025, the amount of the obligations was estimated at 48 billion rubles (2.2 bAED / 4.1 bCNY / 55 bINR). Payment will be made in Russian rubles with the consent of the Russian government. The decision on the payment structure was agreed upon on the eve of Vladimir Putin's visit to Delhi in early December 2025.

The share of the Japanese consortium SODEXO and the accumulated dividends are also held in pledge until the accumulated funds of the project's liquidation fund are transferred to the Russian account and Japan returns the seized Russian state and private funds held in Japanese banks.

Vankor Cluster and Vostok Oil

20 years ago Rosneft started development of Vankor project, large-scale promising fields in Eastern Siberia. To develop Vankor oil and gas condensate field, unique in terms of reserves, a subsidiary company Vankorneft was established. The project is equipped with the most modern and advanced engineering solutions in the field of oil and gas production, treatement and transportation. More than 95% of the equipment and technologies used at Vankor project are of Russian origin. Oil recovery factor at Vankor is one of the highest in Russia. Project's utilization rate of associated petroleum gas is almost 100%. To achieve maximum synergy, the project pioneered cluster development of nearby Suzun, Tagul, and Lodochnoye fields.

Since 2016, Indian companies (ONGG, Oil India Limited, Indian Oil Corporation, and Bharat Petroleum) own 49.9% of Vankorneft.

In 2019, Vankor cluster became part of Rosneft's flagship project, Vostok Oil, the largest investment project in the global oil and gas industry. Vostok Oil includes 52 licensed areas in northern part of Krasnoyarsk Krai and Yamalo-Nenets Autonomous District, where 13 oil and gas fields are located. The renewed project includes the development of the following main fields:

The already being developed Vankor cluster (Vankor,Suzun, Tagul, Lodochnoye,Ichemminskoye),

Payyakhskoye field and the Zapadno-Irkinsky subsoil area,

Vostochno-Taimyrsky cluster.

Vostok Oil project, controlled by Rosneft, is the largest growth point for oil production in Russia in the near future. The project's resource base exceeds 6.5 billion tons of premium light sweet oil (40 API degrees, 0.02% sulphur).

In 2020, Vankor cluster produced 11.3 million tons of oil.

At the end of 2020, Rosneft sold 10% of Vostok Oil project to international trader Trafigura for 630 billion rubles (in equivalent).

09.04.2021 PJSC “Rosneft” transferred its stake in Vankorneft JSC, which the company owns jointly with the Indian consortium, to Vostok Oil.

In 2022, Trafigura sold its 10% stake in the project to an Azerbaijani businessman's oil trading company registered in China (Nord Axis).

As of 2025, preparatory work is underway for construction of oil collection and processing facilities, 770-kilometer Vankor-Payyakh-Bukhta Sever oil pipeline, and Bukhta Sever oil terminal.

Scheme of Vostok Oil project

The first stage of the port's construction provides for the possibility of loading up to 30 MTPA of oil. Initially, this target volumes were scheduled for 2024. As of June 2026, start of crude oil export is scheduled for September of 2026.

By 2030, after commissioning of the second and third stages of construction, volume of oil production and supply will reach 115 million tons per year (315 ktd).

Gas condensate production

Key gas condensate production centers:

Nadym-Pur-Tazovskiy group of fields (Gazprom)

Astrakhanskaya group of fields (Gazprom)

Urengoy group of fields (Rospan - Rosneft)

Arctic offshore fields (Novy Port - Gazprom Neft)

Yamal group of fields (Yamal LNG and Arctic LNG 2 - Novatek)

Oil and gas condensate grades

Key grades of oil and gas condensate:

Urals (at the exit of the Transneft pipeline system in the European part of Russia)

ESPO blend (at the exit of the Eastern Siberia-Pacific Ocean pipeline)

CPC blend (Caspian Pipeline Consortium)

Siberian light

Sakhalin blend

Sokol

Varandey blend

Taxes

Mineral extraction tax (MET) is the leading oil and gas tax in Russia.

In 2024, MET of oil production amounted to 10.1 trillion rubles, MET of gas condensate production - 675 billion rubles. In total, this is equivalent to 29.4% of the federal budget revenues.

Since 2023, oil and gas companies have been paying an additional income tax on net profit of oil and gas companies. In 2024, this tax amounted to 2 trillion rubles (5.4% of the federal budget's revenues).

International organizations

Russia is a member of OPEC+ and BRICS.

Since 2020, voluntary oil restrictions jointly implemented with OPEC countries have effectively managed spot supply of oil on international sea-born market and, consequently, overall price level.

Oilfield Service

Reorganization of Russian oil services industry since 2022

2022 has significantly changed Russian oilfield services market. Western oilfield services companies have started to wind down their activities in Russia, which has had an impact on the volumes of oilfield services and at the same time given a boost to the development of domestic oilfield services. Traditionally, restrictions on the provision of oilfield services are one of the foundations of US pressure on disloyal oil-producing countries. In addition to Russia, such tactics are applied to Iran and Venezuela (before the coup in January 2026).

Restructuring of Russian oil services to import-substituting goods and services has led to high industrial inflation in the oil industry. This inflation is significantly higher than consumer inflation.

Another negative development was the departure of Ukrainian shift workers from North fields. Traditionally, Ukrainian oil service workers have made up a significant portion of shift workers in Yamalo-Nenets Autonomous Okrug and Khanty-Mansi Autonomous Okrug since Soviet times.

Technological Challenges of Russian Oilfield Services

As of 2026, the Competence Center for Technological Development of the Fuel and Energy Complex under the Ministry of Energy of the Russian Federation notes the following challenges in using current technologies of Russian oilfield services companies:

The multiplicity and resolution of seismic data are insufficient for the development of complex reserves, including those with a thickness of less than 10 meters.

New methods of geophysical research are required

Need to increase reference database for current fields for purposes of geological modelling

Need to model multiphase media

Need to develop measuring devices and sensors for hard-to-recover conditions

Need for complex solutions to maintain oil production levels

Need to develop mobile, modular solutions for onshore infrastructure

Creation and development of offshore production systems, including underwater systems

Low penetration in hard-to-recover formations

Need to improve the accuracy of wellbore guidance

Need to improve the accuracy of drilling mode control (pressure, density, and speed)

Need to significantly increase number of stages and volume of hydraulic fracturing

Involvement of laminated formations

Regulation of well operation

To overcome these challenges, it is necessary to develop the following domestic solutions based on available and promising Russian technologies:

Seismic surveys with 50,000 channels or more, pulse sources, and autonomous geophones

High-latitude geophysical well surveys for use in polar and subpolar regions

Geophysical well surveys with boundary and lithography mapping

Creation of a “digital core”

Multiphase flowmetry

3D geomechanical modeling

Technologies of thermochemical influence on the reservoir

Surfactants (surface-active substances) - polymer and alkaline flooding

Underwater production complexes and underwater booster compressor stations

“Digital drilling rig” - a complex of interconnected ground, well, and digital systems and special software

Ice-resistant mobile drilling rig

Solutions for multi-stem wells with separate production

Solutions for repeated hydraulic fracturing with crack reorientation

Solutions for intelligent well completion

Development of solutions for associated production of lithium, helium, and rare-earth metals

Pipeline Transportation of Oil

Oil transportation industry is one of the components of Russian oil industry. State-owned Transneft is natural monopoly in this industry. Unlike USA Russia has a centralized system for transporting crude oil and refined products, which improves efficiency of using oil pipelines. Transportation tariffs are usually indexed according to “Inflation minus” principle, which allows for containment of transportation tariffs even in ruble terms. Another advantage of the natural monopoly in oil transportation is creation of a centralized and large order for necessary equipment and IT systems, which has ensured a 95% level of domestic equipment used by this monopoly.

Some of the key projects of Russian Federation era include:

Caspian Pipeline Consortium pipeline, which supplies oil from Caspian fields of Kazakhstan and Russia to port of Novorossiysk in Black sea.

Eastern Siberia-Pacific Ocean pipeline, which supplies Eastern Siberian oil to ports of Primorsky Krai and through Skovorodino-Mokhe branch to China.

Pivot to Asia of Russian economy requires modernization of Russian oil pipeline system. Transneft is actively increasing factual capacity of existing oil pipelines that supply crude oil to Black Sea and Far Eastern oil terminals.

Sea-born Crude Oil Export

Emergence of Russian tanker fleet

The first oil tanker sailed in Russia was Zoroastr. It was built in 1878 by order of Branobel at a Swedish shipyard.

The first domestically built tankers were Skif, Sarmat, and Vandal, which were built at Sormovo shipyard in Nizhny Novgorod region.

Oil transportation during Russian Empire was a sailing of tankers on domestic rivers and lakes.

World War II

In 1942, when German troops reached Caucasus, USSR faced a severe fuel crisis. Main transportation artery, Volga river, was cut off, and railway connection through Rostov-on-Don was disrupted. Region of Baku was home to vast reserves of oil that could not be transported to central regions of the country. To overcome this situation, an unprecedented engineering solution was implemented: railway tank cars designed for transporting oil overland were converted into floating vessels. They were filled with oil to about two-thirds of their volume (to ensure floating), connected into long trains of 15-20 units, and towed across Caspian Sea. From Baku, the caravans traveled to Krasnovodsk (now Turkmenbashi, Turkmenistan) and Guryev (now Atyrau, Kazakhstan). This was the only remaining route for exporting strategic raw materials. At the ports of arrival, the tanks were lifted out of the water, placed back on railway trolleys, and sent further by rail through Central Asia (Tashkent) and Kazakhstan to central part of the country, primarily to Saratov Oil Refinery.

Post-war period

During USSR era, absolute priority in oil supply area was to meet needs of its own economy. After WWII crude oil began to be exported to Eastern Europe. All exports were carried out through oil pipelines. Maritime transportation of oil was not significant in that time.

Export of Russian oil by Greek shipowners

Greeks are historically one of the main shipowners in the world. It was two Greek businessmen Aristotle Onassis and Stavros Niarchos who created the modern maritime oil trade after the end of World War II.

Thanks to geographical and cultural proximity Greek companies actively participated in Russian oil export from the beginning. Initially Russian sea-born crude oil exports headed to Western and Southern Europe.

Greek shipowners has continued to export Russian oil after beginning the special military operation on 24.02.2022, avoiding pressure from USA, UK and EU. Export of Russian oil is currently one of the main pillars of Greek shipowners' wealth. Shipping industry accounts for 12% of Greece GDP.

The largest Greek tanker shipowners in 2025 were:

Angelikoussis Shipping Group, controlled by Maria Angelikoussis (daughter of John Angelikoussis)

Dynacom, controlled by Georgios Prokopiou (manages around 173 tankers)

Capital Ship Management, controlled by Evangelos Marinakis

Thenamaris, controlled by Konstantinos Martinez (manages 89 tankers)

Almi Tankers (operates about 13 tankers)

IMS, controlled by Marios Gialozoglou

Latsko Shipping, controlled by Marianna Latsis

Minerva Marine, controlled by Andreas Martinou

Delta Tankers, controlled by Diamantis Diamantides”

Evaland Shipping, controlled by Nikos Kefalas

Capital Products Partners, controlled by Ioannis Papalekas

Polembros Shipping

Atlas Maritime Transport

Roxana

World Shipping Corporation

Westport Tankers

Share of EU shipowners in Russian oil exports has been declining since Q2 2023. Thus, share of Greek shipowners (leading owners, commercial and technical managers of EU tanker fleet) decreased from 33% of the total volume of Russian crude oil and dirty products sea-born export in May 2023 to 8% in September 2024. However, Greek shipowners continue to participate in export of Russian light products, with their share decreasing from 40% in Q2 2023 to 24% in September 2024, but it is still remaining relatively high. After marker prices drop in Q2 2025, the share of Greek shipowners began to grow again.

In May 2025, the share of Greek shipowners in export of Russian oil was estimated at 25%. The share is decreasing due to pressure from European Commission.

Freedom Fleet

To ensure crude oil exports, Russian and neutral commodity traders, Russian upstream companies formed their own tanker fleet in 2022, which can be called Freedom fleet as it gives sovereignty for Russian to operate in international markets.

Russia thanks to being in centre of Eurasia always relies predominantly on land-based transportation. As of now we observe hyperactive process of building own maritime trade and creation of required infrastructure. Western countries have been going through this path for centuries. China, thanks to gigantism and tough centralization, mastered this path in two decades.

As of Q3 2024, the fleet involved in Russian crude oil and fuel oil export consist of 410 tankers. Of these, the majority are Aframax-class tankers.

Major addition to the tanker fleet exporting crude and dirty products occurred in Q2 2023 (an increase of 25 vessels per month) and in December 2023 (an increase of 7 new vessels). The tanker fleet exporting light and middle distillates (diesel fuel, gasoline, naphtha) was actively replenished in April 2023 (70 tankers) and later in May-July (20 tankers per month).

Since 2024, tankers involved in export of Iranian and Venezuelan oil have also been used to export Russian oil. This trading strategy was utilized even in March 2022, but was not relatively popular - market share was only 4%. In September 2024, market share of this trading strategy reached 35% of the total volume of sea-born crude oil export. Underlying tanker fleet amounted to 155 tankers.

In the summer of 2024, share of Aframax-class tankers involved in the export of Russian crude oil and petroleum products reached 34% of the total number of vessels of this class worldwide. In the medium-range (MR) class, the share of tankers exporting Russian crude oil and petroleum products in the summer of 2024 was 15%.

All of this lead to a deepening division of the international oil fleet into a Western part controlled by Washington, London, and Tokyo, and an Eastern part controlled by Russia, Iran, previosly Venezuela and to some extent China. From a commercial perspective, the Eastern fleet operates within its own balance of supply and demand, but it is still in the process of forming a common set of institutions for all countries, including maritime insurance and reinsurance, technical management, and financial settlement systems. However, the formation of such institutions is actively underway, both from below (based on the daily operational work of companies involved in trade) and from above (mainly based on the BRICS platform). Attack of USA to Venezuela and Iran in 2026 lead to changing of way to export Venezuelan oil and temporarily diminshed Iranian flows. That made a hit on such trading strategy of independent tanker fleet.

USA, UK, EU as well as occasionally some of their satellite countries, have added tankers involved in the export of Russian hydrocarbons to their blacklists. Usually, initial recovery after each package affecting the fleet takes about two months. During this period of time new tankers are purchased and sailed to the trading regions, new agreements with buyers on logistic schemes are reached. Full recovery takes about four to five months. Market participants have already learned how to react to these packages, but each package brings certain losses to all Russian participants in export schemes.

European pirates

EU, UK, Norway use piracy practices of seizures of Russian merchant vessels in neutral waters of adjacent seas.

List of incidents:

28.12.2024 - tanker Eagle S (9329760) was captured in international territorial waters and escorted into Finnish territorial waters. On 03.02.2025, the tanker and the cargo was released. The plans to steal the cargo were eventually revised and canceled.

21.01.2025 - container ship Baltic Summer (8802090), with a crew from Russia and Belarus, was detained off the coast of Portugal. The ship's owners were suspected of smuggling drugs from South America. The container ship was held in the port for three days, with the crew threatened with weapons and prevented from contacting the consul. In the end, the security forces found nothing but bananas and mangoes. They completely disrupted the cargo, and as a parting gesture, they took away the cigarettes and money.

26.01.2025 - bulk carrier Vezhen (9937270) was captured in international territorial waters and escorted to Swedish territorial waters. On 03.02.2025, the vessel was released.

30.01.2025 - Norwegian Coast Guard detained vessel Silver Dania (8808604) with a Russian crew on board. The reason given was that the vessel may have been involved in an incident involving the damage of a fiber-optic cable in the Baltic Sea between Latvia and Sweden. Subsequently, the Swedish authorities refuted their own accusation. On 01.02.2025, the vessel was released.

21.03.2025 - Germany decided to steal tanker Eventin (9308065) with a cargo of fuel oil from Ust-Luga. In January, after a breakdown in neutral waters, it was towed to German port of Sassnitz. It was later added to its “sanctions" list by European Commission, and on this basis, German authorities decided to confiscate it. As of 18.03.2026 the tanker still in the port of Sassnitz.

11.04.2025 - capture of Aframax class tanker Kiwala (9332810) by Estonia.

13.05.2025 - an attempt to seize Aframax class tanker Jaguar (9293002) by Estonia with support of Polish Air Force. The attack was repelled due to courage of vessel crew timely arrival of Su-35 of Russian Aerospace Forces.

27.09.2025 - seizure of tanker Boracay (9332810) by French military and detention of two crew members. On 03.10.2025, the vessel left French territorial waters. French President Macron explicitly stated that the goal was to detain tankers on their way for 1-2 weeks on false charges in order to disrupt the transportation of Russian oil.

In November 2025, there were reports of British Royal Marines Special Forces training on the Estonian island of Saaremaa to capture ships and oil platforms near Russian territories.

In February 2026, Ireland passed a “law” that would allow Irish troops to seize Russian tankers. This is a continuation of EU's strategy to block Russian hydrocarbon exports through Baltic Sea. UK and France have already taken similar actions, making it difficult for vessels to pass through English Channel.

06.03.2026 - Sweden seized cargo vessel Caffa (9143611).

13.03.2026 - Sweden seized tanker Seaowl I (9321172).

20.03.2026 - France has detained tanker Deyna (9299903).

03.04.2026 - Sweden seized tanker Flora I (9307815).

03.05.2026 - Sweden detained tanker Jin Hui (9430272) in its territorial waters.

01.06.2026 - France detained tanker Tagor (9282481) in the international waters of North Atlantic.

14.06.2026 - UK detained tanker Smyrtnos (9389100) in La Manche.

22.07.2027 - EU authorities detained South Star MR tanker (9263186) in Mediterranean Sea off the coast of Tunisia.

Apparently, these actions are a pilot for European countries and will be expanded to all Russian exports in future. Among “reasons” mentioned are “lack" of insurance recognized by London, age of vessels, and portcalls to Russian ports. Unfortunately, there has been no response from Russian military so far.

Increase in the number of military seizures of commercial vessels in 2025-2026 indicates sovereigntization of Russia's international trade. Creation of foreign trade mechanisms that are resistant to Western pressure has led to need for military involvement by West countries.

Maritime insurance

Problem of pressure by US, UK and EU on Russia's international trade is key for Russian international cargo export. First of all, it affects maritime trade of large cargoes, such as oil, LNG, LPG, coal, fertilizers, wheat, container transportation. For the West, Russian maritime trade is easier to control than overland trade. Pressure on insurance industry is one of the main ones, along with pressure on flag countries and second only to pressure on banks and payment intermediaries.

The following aspects can be identified as subproblems:

· Refusal to insure maritime cargo transportation by common for the industry UK (and other Western) insurance companies if the price exceeds so-called "price ceiling".

· Refusal to reinsure risks associated with Russian maritime transportation by Western reinsurance companies.

· Refusal to insure ships by mutual P&I clubs.

· Overcharging of additional military premiums.

· A realistic default of Western insurance companies against Russian companies in the event of an insured event.

Cargo insurance

On a loaded tanker, it is the cargo that has the main value. Its value is many times higher than a value of the tanker itself.

As a result of wide-scale British occupation of different parts of the world UK insurance companies have historically been the main maritime insurers, including oil cargo transportation. This was one of UK tool for control over maritime trade after the loss of its colonies after World War II. As a consequence UK also controlled related things such as reinsurance, maritime law, arbitration, analytics.

In 2022-2023 pressure of USA, UK and EU on Russian maritime export of crude oil and petroleum products was initially done through the insurance market. Practical mechanism of this type of pressure is prohibition of insurance companies from insuring transportation of Russian cargo if its price exceeds the so-called "price cap" at loading port. This refusal created short-term operational challenges for Russian shippers and causes moderate decrease of profit of insurance companies in UK and other Western countries due to a further decrease in their share in the insurance of global oil and petroleum product transportation.

Leading post-2022 Russian insurance companies that insure maritime oil transportation:

Ingosstrakh,

SOGAZ Insurance,

AlfaStrakhovanie,

VSK Insurance,

Soglasie.

This segment of Russian insurance business actually emerged in 2022 as a result of practical needs of Russian exporters and government efforts to address this issue.

It is worth noting that India, our a leading consumer of maritime oil exports, has formally added Russian insurance companies to the list of domestically permitted insurance companies, which allows all Indian participants in the supply chain to rely on this and not have to worry about potential risks associated with working with Russian companies at the individual level.

It is also worth noting the creation of phantom Western insurance companies in 2024 that temporarily issued cargo transportation insurance that is recognized by counterparties. The most notable example was the Norwegian insurance company Ro Marin, which was owned by a Russian resident in St. Petersburg. During its existence, it allowed Russian oil exporters to overcome Western sanctions.

UK Insurance companies continue to insure Russian cargoes, provided that it does not fall under an explicit domestic restrictions. However, given that almost all Russian exports have been blacklisted by Western countries, the share of Western insurance companies is minimal as of 2026.

Additional War Risk Premium

Western countries have deliberately declared a significant part of Russian territorial water as a zone with extremely high risks. Even those where there are no military actions at all. Underlying reason is to dramatically increase the cost of insurance premiums for all insurance companies that are willing to work with Russian cargoes, but rely on British analytical data to calculate insurance premiums. It is worth noting the special role of the UK, as its insurance companies are the world leaders in the segment of military risk insurance, and it is the UK that supplies unmanned boats to Ukraine for strikes on Russian infrastructure in Black Sea and Mediterranean Sea, including oil and gas infrastructure.

Mutual P&I Clubs

The second most important insurance is the insurance of the tankers themselves. This risk has historically been insured by mutual insurance clubs, which are owned by the shipowners themselves. The main clubs are located in USA, UK and Japan. There is a club of mutual insurance clubs called the International Group P&I. The members of this club in 2025 are:

Gard P&I Club - Norway;

UK P&I Club - United Kingdom;

North of England P&I Club — United Kingdom;

Japan P&I Club — Japan;

Britannia P&I Club — United Kingdom;

Steamship Mutual — United Kingdom;

Swedish Club — Sweden;

Skuld P&I Club — Norway;

West of England P&I Club — United Kingdom;

Hanseatic P&I Club — Germany;

Korea P&I Club — South Korea;

China P&I Club — China (the only non-Western participant).

The creation of such a club does not pose an organizational and financial problem. However, Western countries put pressure on our foreign contractors to ensure that the vessel for which this type of insurance is issued is insured exclusively by a club that is part of International Group P&I. All other mutual insurance clubs are considered "bad" by Western countries.

Share of controlled by the West mutual insurance market for ships (International Group P&I clubs) has decreased from 90% to 85% of global tonnage of ships in recent years, and it continues to decline gradually. Therefore, it can be estimated that the share of mutual insurance organizations in the East is around 10-15%. Moreover, most of this fleet that is independent of the West consists of tankers. Therefore, the share of mutual insurance organizations in Eastern countries in oil transportation is significantly higher and can reach up to a third of the operations. It is International Group P&I that is one of the tools of pressure of UK and USA on the other participants of the market. Previously, a tanker having P&I insurance not from International Group P&I had close to zero chances to carry out trade operations on equal terms.

Reinsurance

Refusal of the world's leading EU reinsurance societies to work with Russian insurance companies in 2022 required to create a Russian alternative. The same year capital of Russian National Reinsurance Company was increased tenfold. It created prerequisites for work of Russian insurance companies in maritime transportation. As of 2026 capital of Russian National Reinsurance Company is still not enough to cover all volumes of Russian maritime transportation.

In 2026, an inter-government agreement was reached regarding of work of Russian insurance companies with a Chinese reinsurance company within Russian oil and gas export to China.

Flag States

According to Seala AI, Panama was the leading flag state in oil shipping - as of 27.05.2025, 1451 tankers fly flag of this country.

In May 2025, Panama introduced a mandatory requirement for ships flying the flag of this country to disclose the details of oil and petroleum product transshipment at sea in advance, with a detailed indication of all information. Naturally, ships of the Eastern Fleet will not disclose this information, which will eventually lead to either the voluntary abandonment of Panamanian flag by shipowners or its emergency removal by Panamanian authorities. The tightening of Panama's requirements, which have nothing to do with IMO safety or regulations, is a result of the Trump administration's crackdown on countries. It is worth noting that in January 2025, Trump promised to seize the Panama Canal by force. The Panama Canal is the primary source of revenue for the country, and it would be impossible for it to offer significant military resistance to USA. As a result, the rights of Chinese shareholders in the Panama Canal infrastructure were restricted. Additionally, Panama is required to allow free passage through the canal for US vessels.

As a result, in 2025-2026, Russian fleet shifted away from Panamanian and several other commonly used flags in the industry. This involved switching to rare flags and even creating new flag registries from scratch. This, in turn, was used by EU countries as a reason to detain tankers and cargo ships that they simply did not like.

In June 2026, Russian government began to ease bureaucratic rules for transfer of merchant ships, primarily oil tankers owned by foreign legal entities, to Russian flag. This is the second attempt this year. The first attempt was triggered by global hunt by US Navy for tankers, including Russian tankers, carrying Venezuelan oil. The second attempt was prompted by the increased piracy by EU and UK in Q2 against tankers carrying Russian oil and petroleum products from Baltic Sea ports.

Crude Oil Exports

Russia exports surplus of crude oil.

Oil export volumes by year:

2000 – 144.4

2001 – 164.5

2002 – 189.5

2003 – 228.0

2004 – 260.3

2005 – 252.5

2006 – 248.4

2007 – 258.6

2008 – 243.1

2009 – 247.5

2010 – 250.7

2011 – 244.5

2012 – 240.0

2013 – 236.6

2014 – 223.5

2015 – 244.5

2016 – 254.9

2017 – 252.8

2018 – 260.6

2019 – 269.2 (738 ktd). Maximum export level since 1992.

2020 – 238.6. Export decline due to the pandemic.

In 2021, overall сrude oil export amounted to 229.9 million tons (630 ktd). Countries that later imposed self-restrictions on Russian crude oil imports in 2022-2023 accounted for 54% of Russian oil exports in 2021.

Overal volume of crude oil and petroleum product exports in 2021 was 360 million tons (986 ktd). Geographical structure of Russian crude oil, gas condensate and refined products exports in 2021 was as follows:

EU - 452 ktd.

China - 219 ktd, including oil pipeline supplies.

UK and USA - 82 ktd.

Belarus - 66 ktd.

Türkiye - 27 ktd.

India - 14 ktd.

Africa - 14 ktd.

Latin America - 14 ktd.

Volume of crude oil exports in 2022 was 242 million tons (663 ktd). Despite the pressure from Western countries, oil exports increased.

Following EU's refusal to purchase Russian oil in 2022, as well as political attacks by USA, EU, and UK on logistical routes for exporting Russian oil and its purchase by third countries, as well as the expropriation of refineries owned by Russian companies by national authorities, a structural shift in the international trade of Russian oil occured. Russian state-owned and private oil companies, as well as independent trading companies, have formed their own tanker fleets and are now responsible for full transaction cycle, including sales to foreign refineries, freight, transshipment at terminals, insurance, payments in national currencies, and hedging against price and currency risks. Center of international trade in Russian oil has shifted from Switzerland to UAE.

Volume of crude oil exports in 2023 was 234.3 million tons (642 ktd). The share of countries that have restricted their imports of Russian oil has decreased sevenfold to 8%. China and India account for 57% of the total exports of Russian crude oil. In September 2024, India's share in the maritime export of oil and gas condensate reached 52% of the total volume of oil exports by sea, while China's share was 40%. For comparison, China and India's share in the global population is 35%, and their share in global GDP is 23%.

Overall volume of crude oil and petroleum product exports in 2023 was 375 million tons (1027 ktd). Geographical structure of oil and petroleum product exports underwent significant changes in 2023:

European Union - 82 ktd, including oil pipeline deliveries. All supplies to Russian refineries in EU and other refineries that are technologically dependent on Russian oil. After political attack by EU and Ukraine on Hungary and Slovakia in July 2024 and the interruption of Lukoil's oil supplies to these countries' refineries, Russian oil exports to EU have further decreased.

China - 329 ktd, including oil pipeline and railway supplies.

UK and USA - 0.

Belarus - 66 ktd.

Türkiye - 96 ktd.

India - 260 ktd. Mainly crude oil.

Africa - 137 ktd.

Latin America - 137 ktd. Mainly diesel fuel to Brazil.

Russian Urals grade has been replaced in EU and UK by grades from Brazil, Guyana and Persian Gulf countries. There was also a stagnation in EU and UK refining volumes due to a slight decrease in domestic demand and foreign demand for EU petroleum products.

Volume of oil exports in 2024 was 240 million tons (656 ktd).

Russian oil exports in 2025 amounted to 238 million tons (652 ktd). A 1% decrease over the year.

Pipeline exports

Drizhba (Friendship) pipeline system

Historically, Russia, and previously Soviet Union, was focused on exporting oil through oil pipelines. During Soviet Union era, the world's largest international oil pipeline system Druzhba was built. Crude oil was exported through the system to the countries of the Council for Mutual Economic Assistance, including Hungary, Czechoslovakia, Poland, and German Democratic Republic. The system includes 8,900 km of pipelines (3,900 km of which are located in Russia), 46 pumping stations, 38 intermediate pumping stations, and tank farms that can hold 1.5 million cubic meters of oil. The pipeline helped to export up to 67 million tons of oil (918 ktd) to these countries every year. However, oil exports through Druzhba pipeline have been rapidly declining since 2022. In 2024, total volume of exports through Druzhba was 11.5 million tons. Of these:

4.8 million tons were sent to Hungary.

4 million tons were sent to Slovakia.

2.7 million tons were sent to Czech Republic.

As of January 2025, there were only two key buyers of pipeline oil:

Hungarian MOL that purchases oil for its refineries in Hungary and Slovakia.

Polish Orlen, which purchases oil for its refineries in Czech Republic (Litvinov and Kralup).

It is estimated that the flow of Russian oil to EU through Druzhba pipeline has not exceeded 10 million tons in 2025. Russia-Belarus supply route is now the main one for Druzhba (23 MTPA).

Belarus

Belarus is one of the key consumers of Russian oil. Almost all of crude oil comes through the Druzhba pipeline. Russia is the main, and in recent years the only, supplier of oil to Belarus.

From a legal point of view, Belarus stands a unique position between general rules for exporting Russian oil and internal Russian oil trade, reflecting integration of Belarus and Russia into Union state.

Annual supply volumes are stable at 24 MTPA (66 ktd), of which 23 MTPA via Druzhba (63 ktd) and 1 MTPA by rail.

Supply volumes were minimal in the first quarter of 2020 during the escalation of Russian-Belarusian relations.

ESPO

Main Russian oil pipeline route at the moment is branch “Skovorodino - the border of PRC” (Skovorodino - Mohe) from oil pipeline “Eastern Siberia - Pacific Ocean”. Design capacity of the oil pipeline, launched in 2010, is 30 MTPA (82 ktd). Supplies via this oil pipeline are carried out directly to Chinese refineries in northeast of China. Unlike maritime exports, pipeline exports face fewer political challenges and are more stable.

Kazakhstan

Russian oil also goes to China in transit through Kazakhstan pipeline system.

Design capacity of Kazakhstan-China oil pipeline launched in 2006 amounts to 10 MTPA (27 ktd). Actual capacity as of 2025 is likely to be at least 20 MTPA.

Tariff for oil transit through Kazakhstan in 2026 is 5.5 AED / 13.2 CNY / 1436 INR / 1216 RUB per ton without VAT.

Seller from Russian side is Rosneft. Buyer on Chinese side is PetroChina.

Deliveries by period:

Export of Russian oil through Kazakhstan to China in 2025 was approximately 10 million tons (27.4 ktd).

Forecast for 2026 is 12.5 million tons (34.2 ktd).

In Q1 2026, actual deliveries amounted to 2.5 million tons (27.9 ktd).

Uzbekistan

Russian oil supplies to Uzbekistan amounted to 234 thousand tons in 2024 (0.6 ktd).

Crude Oil and Gas Condensate Refining

Russian oil refining industry is one of the largest in the world in terms of oil refining volumes, as well as one of the largest in Russia in terms of its contribution to the economy.

Oil and gas condensate processing plants

Key oil refineries in Russia:

Rosneft:

Ryazan Oil Refining Company - 17.1 MTPA.

Tuapse Oil Refinery - 12. Has an export profile.

Angara Petrochemical Company - 10.2.

Bashneft-Ufaneftekhim - 9.5.

Komsomolsk Oil Refinery - 8.3.

Novokuybyshevsk Oil Refinery - 7.9.

Bashneft-UNPZ - 7.5.

Achinsk Oil Refinery - 7.5.

Novo-Ufa Oil Refinery (Novoil) - 7.1.

Syzran Oil Refinery - 7.0.

Saratov Oil Refinery - 7.0.

Kuybyshev Oil Refinery - 7.0.

Nizhnovartovsk NPO - 1.6.

Lukoil:

Lukoil-Nizhegorodnefteorgsintez in Kstovo - 17.0.

Lukoil-Volgogradneftepererabotka - 14.8.

Lukoil-Permnefteorgsintez - 13.1.

Lukoil-Ukhtaneftepererabotka - 4.2.

Gazprom Neft:

Omsk Oil Refinery - 22.0. The largest oil refinery in Russia in terms of processing volumes.

Moscow Oil Refinery - 12.

Gazprom:

Gazprom Neftekhim Salavat - 10.0.

Surgut Condensate Stabilization Plant - 4.0.

Astrakhan Gas Processing Plant - 3.3.

Novourengoy Condensate Preparation Plant for Transportation - 0.4.

Safmar:

Apipsk Refinery - 7.0. Focused on export.

Orsknefteorgsintez - 6.6.

Krasnodarsky Refinery - 3.1.

Neftekhimservice:

Yaysky Refinery - 3.3.

Anzhersky Refinery - 1.2.

Other:

Kirishinefteorgsintez (Surgutneftegaz) - 21.

Taneko (Tatneft) in Nizhnekamsk - 16.2.

Yaroslavnefteorgsintez (Slavneft - a joint venture between Gazprom Neft and Rosneft on a parity basis) - 15.7.

TAIF-NK (Sibur) - 8.3.

Tyumen (Antipinsky) Refinery (Rusinvest) - 7.9.

Ilsky Refinery - 6.6.

Khabarovsk Refinery (Independent Oil and Gas Company) - 5.0.

Novoshakhtinsky Oil Products Plant (Peton) - 5.0. Two stages of primary oil refining of 2.5 million tons each have been implemented. The project of the third stage of the plant has passed the state expertise.

Slavyansky Refinery (Slavyansk ECO) - 4.0.

Mari Refinery (transferred for debts to the Moscow Credit Bank) - 1.4.

Usinsky Refinery (Yenisey LLC) - 1.0.

Diteko Refinery (MFC Kapital LLC) - 0.9.

Kochenyovsky Refinery (VPK-Oil LLC) - 0.7.

Nikolaevsky Refinery (Samaratransneft-Terminal LLC) - 0.5.

Itatsky Refinery (Kuznetsky Ugol LLC) - 0.5.

Strezhevsk Oil Refinery (Tomskneft) - 0.3.

Kosobrodsky Oil and Bitumen Plant (a joint venture between Financial Innovations LLC and Energoservis LLC on a parity basis) - 0.2.

Overall capacity of the refineries is over 341 million tons of oil and gas condensate per year, which is equivalent to 934 ktd.

Russia also processes oil and condensate at small refineries with local consumption of petroleum products. These petroleum products are not available on the general market.

Development of new oil and gas condensate processing plants

In 2026, plans were announced a plan to build a new refinery with a capacity of 7 MTPA in Khabarovsk Krai by 2032.

Also in 2026, revival of Rosneft's previously suspended strategic project to establish Eastern Petrochemical Company in Nakhodka (Primorsky Krai) - an oil refinery with a capacity of 12 MTPA and a petrochemical plant with a capacity of 3.4 MTPA - is being discussed.

It is also worth noting the following potential need for development of oil and condensate processing capacities:

Expansion of primary oil processing capacities at existing refineries in North-West of Russia. Cost of shipping of oil from Baltic Sea ports to the buyer countries (India, China) is the highest among all Russian oil export destinations. Combined with discounts on Russian oil at buyer's ports and additional delays caused by EU and UK piracy (even without consideration of complete blockade of Baltic Sea), as well as cost of transporting oil through Transneft system and transshipment at the port, it is questionable whether it is economically feasible for an oil producer to export oil through this route. At the same time, it is these regions of Russia that face seasonal problems with fuel supply during summer months after attacks by Ukraine, USA and UK on Russian oil refineries. In mid-term, cost of oil production in European part of Russia will increase as the share of hard-to-recover reserves grows. Demand for automotive and aviation fuel in this region (Moscow and St. Petersburg) will increase in one way or another once the problems with production of passenger cars and civilian aircraft are resolved. Therefore, with a horizon of 4-5 years, it will be more cost-effective to process and sell petroleum products locally in this region, rather than transporting them by sea to India or China.

Processing of gas condensate from Yamal and Sakhalin gas projects of Novatek and Gazprom in Russia. Previously, condensate from Yamal was exported to Netherlands and processed at an oil refinery where Lukoil had a 45% share. In February 2026, Lukoil was stripped of this share. The condensate from Arctik LNG-2 has not yet been sold due to the plant's downtime. Sakhalin condensate is being sold to a wide range of buyers in Asia. However, the demand for light petroleum products, particularly gasoline, which is the main product of condensate processing in Russia, remains high. It makes practical sense to build a gas condensate fractionation plant on the site of one of the LNG plants to process these volumes locally.

Refining volumes

In 2023, oil refining volumes amounted to 275 million tons per year, which is equivalent to 753 ktd. Utilization rate of oil refining capacities was 81%. Ukraine's attacks on Russian oil refineries had a negative impact on the volumes of oil and gas condensate refining and production of marketable petroleum products in H2 2023.

In 2024, Russia's primary oil refining capacity reached 266.5 million tons of crude oil, equivalent to 728 ktd.

Main petroleum products produced at Russian refineries as of 2024 are:

Diesel fuel - 266 ktd.

Gasoline - 119 ktd.

Fuel oil - 109 ktd.

Naphtha - 59 ktd.

Kerosene - 31 ktd.

Russian refineries performed long-term modernization campaign of their secondary oil refining processes. This increased processing of straight-run fuel oil into useful and relatively scarce gasoline and kerosene. Over the ten years from 2015 to 2024, while overall volume of oil refining remained unchanged, production of commercial fuel oil at refineries decreased by almost half, from 192 ktd in 2015 to 109 ktd, while production of diesel fuel increased by 43 ktd, gasoline by 13 ktd, and kerosene by 3 ktd.

This transformation of the structure of oil product production is extremely necessary in the context of external restrictions on Russian fuel oil in export markets, as well as the growth of domestic consumption of motor fuel and the emergence of temporary shortages of it.

Naphtha balance:

Production – 22 million tons per year in 2023 (60 ktd).

Almost all of the produced commodity naphtha is exported.

Gasoline balance:

Production is expected to reach 44 million tons in 2023 (121 ktd), including the processing of oil and gas condensate. The processing of condensate plays a significant role in the overall production of gasoline in the country. In 2025, production is projected to reach 43.6 million tons (119 ktd). The share of AI-95 in the production structure is expected to increase from 39% in 2022 to 47% in 2025.

Domestic demand is 38 million tons in 2023 (104 ktd). It is the availability of gasoline that causes the main concerns of the Government of the Russian Federation. Therefore, even gasoline exports, which are so insignificant in the Russian oil industry, are often limited by government decisions in order to saturate the domestic market and keep down prices for motor fuel. 97% of the fleet of private passenger cars has gasoline engines.

Net exports amounted to 6 million tons in 2023 (17 ktd), including exports by sea to foreign countries and exports by rail to neighboring countries.

The highest demand for gasoline is observed in the summer, during the peak of the car season. It is during these months that the surplus of production over domestic consumption is at its lowest. In the event of high downtime due to attacks by Ukrainian drones, the surplus may become zero, as was the case in the summer of 2025.

Kerosene balance:

Production – 11 million tons in 2023 (30 ktd).

Domestic demand – 9.5 million tons in 2023 (26 ktd).

Net exports – 1.5 million tons in 2023 (4 ktd).

Diesel fuel balance:

Production – 99 million tons in 2023 (271 ktd).

Domestic demand is 53 million tons in 2023 (145 ktd).

Net exports are 46 million tons in 2023 (126 ktd).

Fuel oil balance:

Production is 44 million tons in 2023 (121 ktd).

Domestic demand is 10 million tons in 2023 (27 ktd).

Net exports are 34 million tons in 2023 (94 ktd).

Bitumen balance:

Bitumen production is about 2 ktd.

Domestic market is 1 ktd.

Export is 1 ktd.

Consumption of oil products

Vehicle fleet and automobile fuel

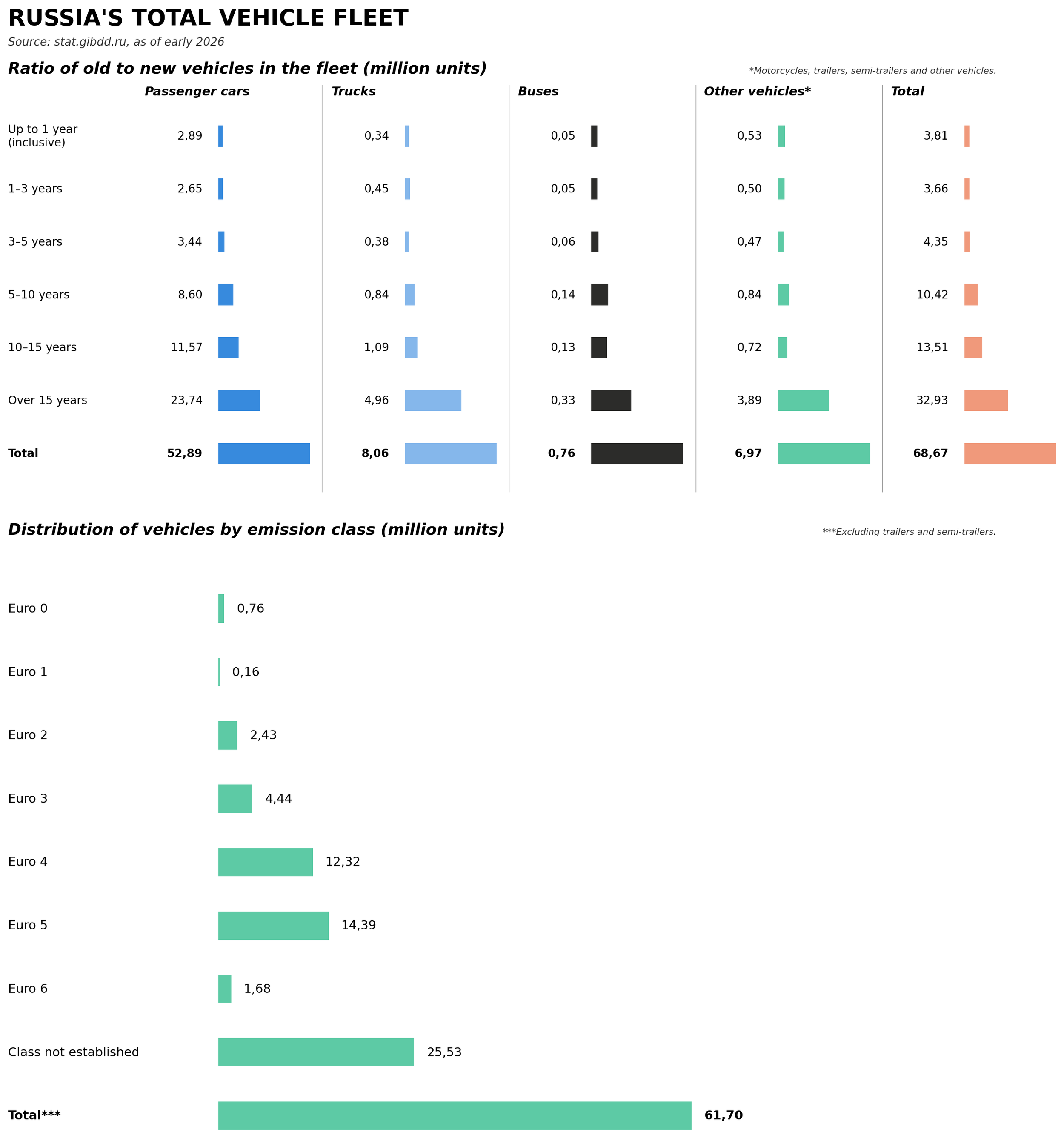

According to State Traffic Inspection (GAI), as of 01.01.2026, there were 68.7 million vehicles registered in Russia, of which:

cars, including passenger cars for commercial purposes, - 52.9 million;

trucks - 8.1 million;

buses - 757 thousand;

others - 7.0 million.

Since 2022, the size of the fleet has been stable and has not increased. The key reasons are the difficult economic situation, the high interest rate on car loans, and the restructuring of Russian car manufacturers to new technical solutions and supply chains. In 2025, the overall fleet decreased for the first time in many years, albeit by a symbolic amount.

Russian car fleet as of 01.01.2026

Gasoline (AI-92-K5 and AI-95-K5) is the dominant fuel for passenger cars (92%).

Diesel fuel (K5) is the dominant fuel for trucks and buses. Diesel fuel is available in seasonal versions - summer, off-season, winter, Arctic.

There is state program for gasification of vehicle fleet. Majority of cars are being transformed to bi-fuel with LPG being the key road fuel. Compressed Natural Gas has lesser popularity. As part of the 2026 fuel crisis, the transition to gas and, to a lesser extent, electric vehicles began accelerating in the summer of 2026. The estimated transition to bi-fuel version is 500-1000 used cars per day.

As of 2026, Russia has an environmental class of K5, which is equivalent to Euro-5.

Additionally, some manufacturers (such as Taneco) produce automotive fuel that meets Euro-6 standards, but it is technically classified as K5 due to the absence of K6 at the current time.

In July 2026, a temporary (until December 2026) relaxation was introduced for gasoline producers, allowing them to sell gasoline labeled K5 in Russia, but with decrease of factual fuel quality up to Euro-3 standard.

A number of mini-refineries produce automotive fuel with an environmental class lower than K5. These refineries are typically located in areas where oil is produced. This fuel is not available on general market for petroleum products and is sold locally to specific consumers.

A number of manufacturers, mainly in Krasnodar Krai, produce technical grades of gasoline that are exclusively exported. These grades do not comply with domestic technical regulations and are not available on the domestic market.

However, out of overall fleet of vehicles (61.7 million), only 16.1 million require fuel of the K5 (Euro-5 and Euro-6) environmental class. More than half (33.3 million) can safely run on K3 fuel.

Exchange trading

In Russia, there is exchange trading of petroleum products. The main and, in fact, the only trading platform is Petersburg Exchange (formerly SPbMTSB). All instruments have physical execution, which minimizes speculation in the market. According to the legislation, oil refining companies are required to sell part of produced light petroleum products on the exchange (as of 09.07.2025, about 15% of gasoline and 12% of diesel fuel).

In H1 2025, volume of exchange trading in petroleum products amounted to 18.8 million tons. Annual growth rate was 3.2%. This is equivalent to 103 ktd or 26% domestic gasoline and diesel production volume. In monetary terms, the exchange-traded volumed in 2025 is estimated at 2 trillion rubles, which is 1% of Russia's nominal GDP in 2025.

The exchange has introduced restrictions on price dynamics during trading sessions for the main types of petroleum products. As of March 25, 2026, maximum increase in an order for the main types of petroleum products is only 0.01% of the last price of a product (previously, it was 0.05%). These restrictions apply to AI-92 and AI-95 gasoline, as well as inter-seasonal and summer diesel fuel. Additionally, the exchange has introduced and regularly tightened restrictions on the ability to place orders for the purchase of resources. This led to a mismatch between exchange quotes and wholesale market prices. The inability to freely purchase fuel on the exchange resulted in an increase in the margin in the next segment, which involved the wholesale resale of the resource.

In July 2026, the standard for selling gasoline on the exchange was reduced from 15% to 10%. This measure will remain in effect until September 2026.

Aspects of domestic market regulation

In the second half of 2023, there was a shortage and a rapid increase in the prices of motor fuel, which led to the escalation of the issue to the level of the Government and the President of the Russian Federation, temporary partial export restrictions and manual management of the industry. Similar problems with the planned fuel supply arose in March 2024. To overcome them, restrictions on exports (gasoline) were also introduced and increased transparency in domestic sales (increasing the share of SPb MTBF sales for diesel fuel). Among the immediate reasons, the following key ones are worth noting:

The tax maneuver to avoid export duties on the export of petroleum products in favor of the mineral extraction tax contributes to the comparison of domestic prices with international ones, minus the cost of logistics.

Temporary reduction in payments for the damper.

Weakening of the ruble exchange rate in international currencies.

Simultaneous entry into scheduled and emergency repairs of a large number of refineries, including the consequences of Ukraine's attacks on Russian refineries.

High demand for fuel from the Ministry of Defense.

Conventions (“bottlenecks”) on the country's railway network.

To systematically address such issues, which are also observed in neighboring countries, a government program for the construction of new oil refineries in the country is clearly necessary. For the oil companies themselves, building refineries may not be profitable or a priority due to a lack of technological suppliers for the necessary equipment, a lack of economic incentives to reduce the domestic market margin, and a low return on investment in oil refining. However, at the state level, the benefits are obvious: the creation of technological competencies in a key industry, the minimization of social risks in terms of fuel prices, the development of related industries, and the reduction of dependence on India and China in terms of oil exports.

As of 2026, this issue remains relevant in the fuel market. On June 1, 2026, restrictions were imposed on the export of aviation kerosene for the first time, in addition to the existing restrictions on gasoline and diesel fuel.

Fuel blending

In November 2025, the Ministry of Finance abolished the excise tax on ethyl alcohol used in the production of motor fuel. The maximum ethanol content in commercial gasoline was increased from 1.5% to 10%.

As of 2026, use of monomethylaniline is temporarily allowed. In 2016, its use was prohibited due to environmental risks and concerns about engine damage. Monomethylaniline is a carcinogen. Currently, monomethylaniline content is limited to 1%, and its use requires strict production and laboratory controls.

Taxes

The damper mechanism plays an important role for the economy and the volume of production and sales of petroleum products.

The theoretical goal of this government mechanism is to ensure that there is a full supply of fuel on the domestic market on a daily basis, while also preventing a sharp increase in fuel prices above inflation targets. The mechanism involves compensating oil refiners from the Russian budget for the lost benefits of exporting oil under certain conditions. The set of conditions and the rules for calculating compensation are often subject to changes as part of the government's situational market management. The mechanism is de facto one of the largest cross-subsidies in the country.

The current rules for diesel fuel and gasoline as of March 2024 are as follows:

Oil refining companies are eligible for compensation from the Russian Budget in the following cases:

If they sell at least 50% of their produced gasoline and diesel fuel on the Russian market.

If they sell at least 15% of their produced gasoline and 12% of their produced diesel fuel on the SPbМТСB. Prior to March, the percentages were 13% and 9.5%, respectively.

The average daily actual price of fuel sales on the St. Petersburg Exchange exceeds the Ministry of Energy's target (56,900 rubles per ton for gasoline and 55,200 rubles per ton for diesel fuel) for the reference month.

Consumers (airlines) are the recipients of the aviation kerosene damper. This differs from the automotive fuel damper, where manufacturers are the recipients.

The amount of compensation currently covers the full difference between domestic Russian wholesale prices and the estimated value of the export alternative for each ton of fuel sold on the Russian market. Previously, reduced coefficients were temporarily applied to payments (68% of the difference for gasoline and 65% for diesel fuel) to reduce the overall amount of payments from the state budget and its deficit, respectively.

Taking into account the ratio of market prices, the damper in 2023-2025 is de facto a government payment to oil companies, which is a “reverse excise tax” on petroleum products. In 2024, payments for the damper and investment allowance for oil refineries reached a record high of 3.7 trillion rubles. This is equivalent to 9.2% of the total federal spending.

Thus, the damper has transformed from an initial mechanism for smoothing out market fluctuations into a mechanism for cross-subsidizing within the oil industry.

The damper is paid for by oil companies' mineral extraction tax deductions and accounts for a quarter to a third of the total amount. Along with the export duty on oil, the damper mechanism prioritizes oil refining in Russia for oil companies.

In mid-2025, the Russian government began to gradually reduce its control over regulated prices in the country. It is reasonable to expect a decrease in the actual amount of damper payments in the near future in order to reduce the deficit of the Russian Federation's federal budget. The deficit of the federal budget in 2024 amounted to 3.5 trillion rubles, which is almost equal to the amount of damper payments. Thus, the damper may once again become a mechanism for smoothing out prices rather than directly subsidizing them.

In 2024-2026, there were restrictions on the export of gasoline and, to a lesser extent, diesel fuel. The degree of restrictions varied (by product, type of manufacturer, and export destination), but the domestic market for automotive fuel was largely decoupled from the international market for large-scale maritime fuel supplies. As a result, the purpose of using the damper was largely lost.

Notes:

Detailed data on global oil market is available in Crude Oil and Petroleum Products module of Seala AI Terminal.

Join Seala AI’s Linkedin page to be informed for all new future releases with new dashboards and insights.

Non-mainstream oil and gas news and views are available in Seala AI’s telegram channel.