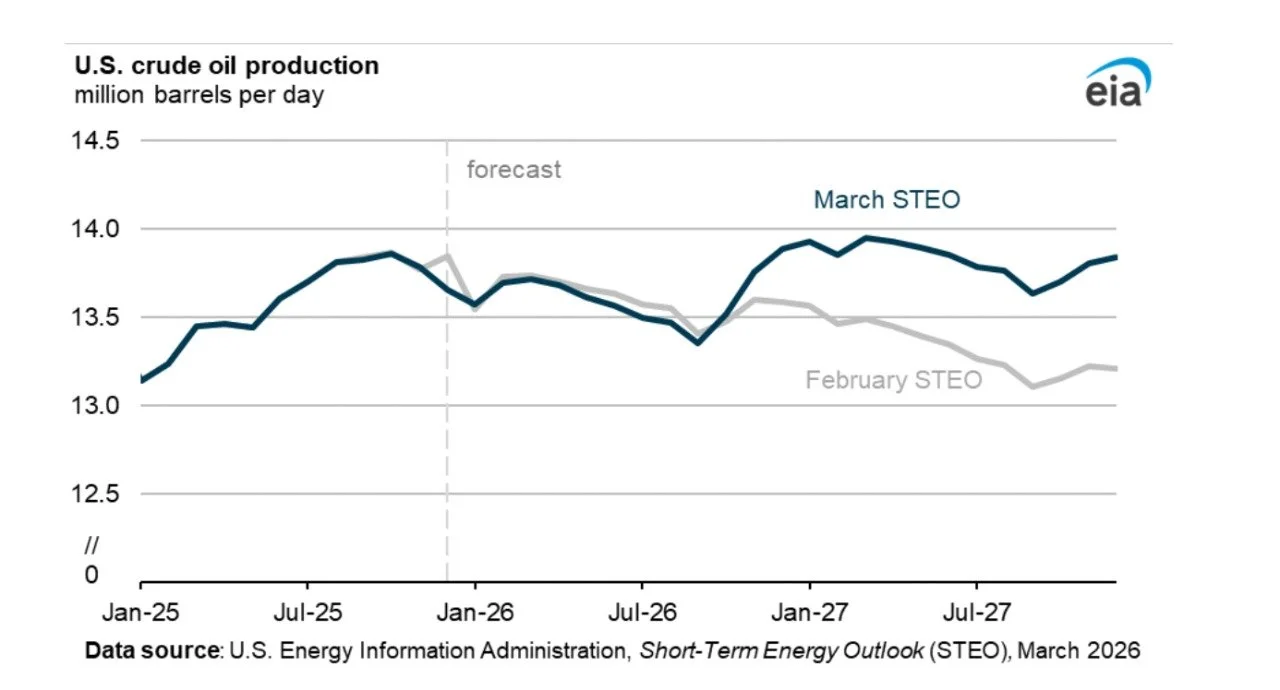

Increase in US crude oil production in DOE STEO

As a result of the Israeli-US attack on Iran and the rise in crude oil futures curves, there has been a change in the economics of new drilling in US shale fields, particularly in Permian Basin. Recent March report from US Department of Energy indicates an increase in planned production compared to February forecast, which starts in Q4 2026.

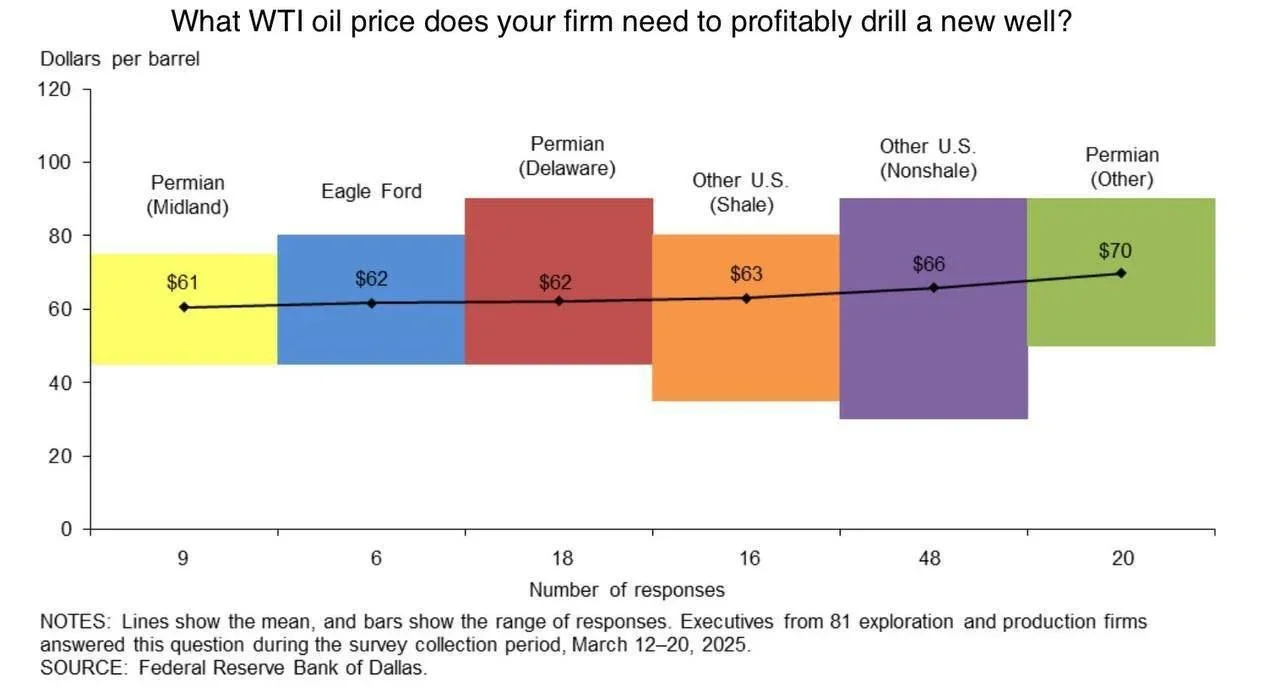

Exactly one year ago, the price at which drilling (!) new wells in Permian basin becomes profitable was in the range of 45-75 dollars per barrel of WTI with an average value of 61 dollars per barrel.

Over the course of the year, the price has naturally increased due to both dollar inflation and the shift to slightly less productive wells than a year ago. It is also worth noting that WTI price is lower than Brent price by the amount of freight cost from Gulf of Mexico (Houston) to North-Western Europe (Rotterdam). Currently, this spead is 1.5 USD per barrel, but it typically ranges from 3 to 5. Therefore, current thresholds for new drilling, converted to Brent index and H2 2026 dollars , can be estimated at 51 (conditionally minimum) - 69 (average) - 83 (conditionally maximum) dollars per barrel.

At current Brent spot price of 96 USD per barrel, the futures curve for Q4 2026 and 2027 is in the range of 82 USD per barrel (October 2026) to 72 USD per barrel (December 2027) per barrel. While not all new wells in Permian Basin will be profitable, share of profitable future wells has significantly increased. This is the driving force behind the increase in crude oil production forecasts for Permian Basin and tUnited States as a whole.

It is also worth noting two moments.

First, OECD decision to release 55 million tons of crude oil from stocks to the market may temporarily reduce market price and will lead to a change in US DOE April forecase. This time, the adjustment will be downward, with April forecast will be between February and March curves.

Second, US shale oil production serves as a natural medium-term defense mechanism against prolonged high prices (100-120+ USD per barrel) in the physical oil market. These additional volumes are not long-term, but they save the market from such shocks with a sharp two-fold increase in the price level. And after the price shock passes, there will be a sharp (within 6-12 months) a decrease in the volume of shale production in the United States.

Notes:

Join Seala AI’s Linkedin page to be informed for all new future releases with new dashboards and insights.

Non-mainstream oil and gas news and views are available in Seala AI’s telegram channel.