Сonsequences of attacks on Iranian South Pars and Qatari Ras Laffan LNG plant

Israel's March 18 attack on Iran's South Pars gas field and Iran's retaliatory strikes on Qatar's Ras Laffan LNG plant, which liquefies gas from the North Field, have significantly reduced the availability of gas in the Asian region.

As a result of the Israeli attack Iranian domestic gas and electricity consumers will suffer. Iran's domestic market is the fourth-largest in the world, after USA, China, and Russia - 265 billion cubic meters per year (BCMA). South Pars accounted for 70% of Iran's gas production (716 mcm/d as of June 2025). As of now there is no information what is remaining production rate and what will be recovery period.

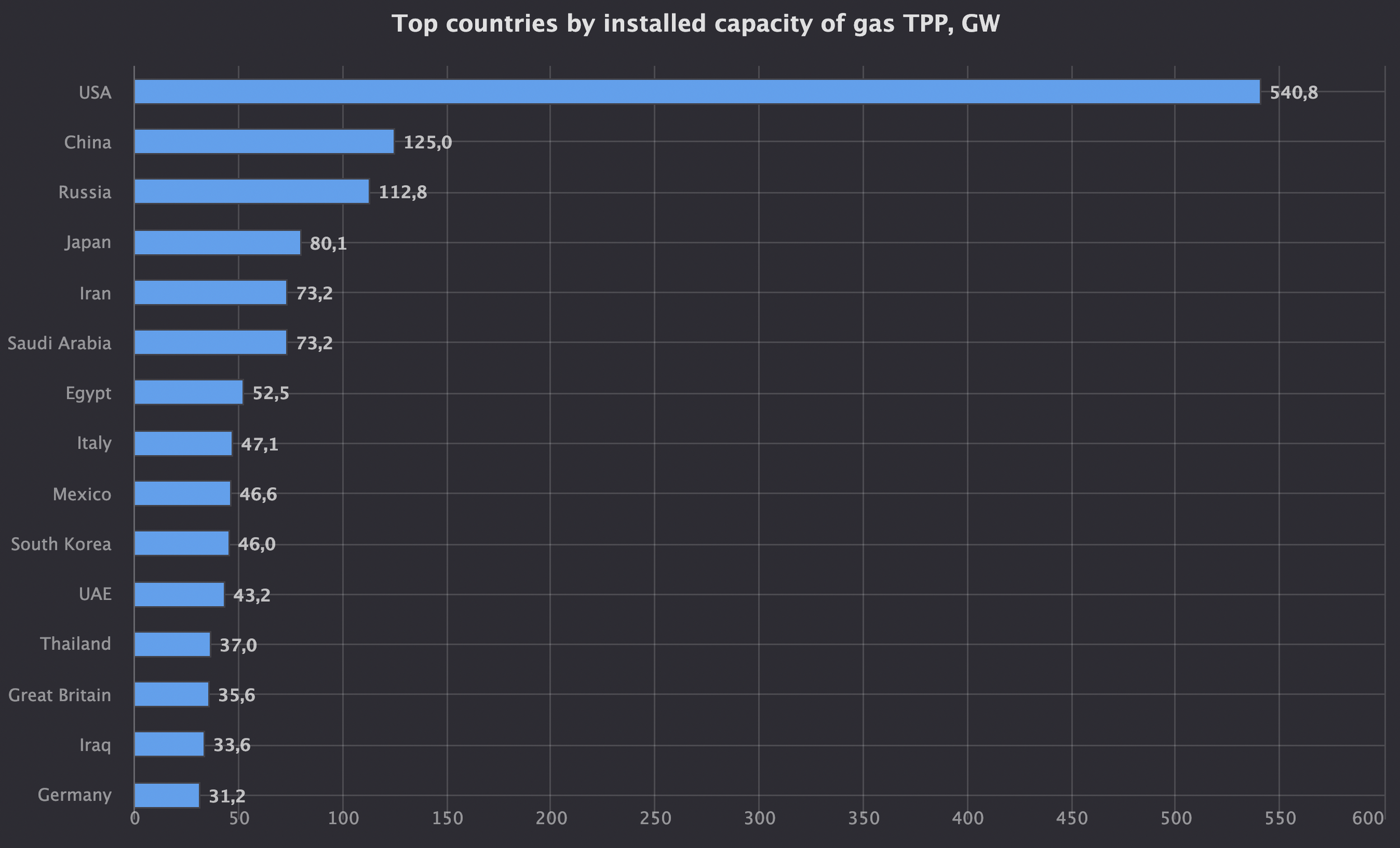

Iran is one of the leaders in gas generation. Installed capacity of gas-fired TPPs in the country is 73.2 GW. Theoretical maximum demand from gas generation is 440 mcm/d. Gas-fired TPPs provides 86% of the country's electricity generation mix. So sharp decrease in gas supply will have immediate effect on domestic power supply.

Iran has also halted gas exports to neighboring Iraq. And could limit or halt supply Türkiye as well.

Gas supply of Iranian gas to Iraq amounted to 55 mcm/d. It is about 40% of Iraqi gas demand. its gas supply, will face an unsolvable problem of not meeting domestic demand during the upcoming heatwave. The country is expected to experience widespread power outages this summer.

Installed capacity of gas-fired TPPs in Iraq is 33.6 GW. Theoretical maximum demand from gas generation is 200 mcm/d. In July and August, everything which could generate electricity, does it. Any disruption in gas supplies leads to a decrease in electricity production by the country's TPPs. In August 2025, due to a 30 mcm/d decrease in Iranian gas supplies to Iraq, there were power outages.

In case of halting of Iranian gas flows Türkiye will be forced to increase purchases LNG on international market. Ability to import additional volumes of Russian gas is limited by its current high utilization rate of both Turkish stream, and Blue stream. There may be an optimization of timing of summer repair campaigns for these gas pipelines. Russia is interested in increasing its gas supplies to Turkey.

However, Ukraine with assistance of UK and USA continues to attack infrastructure of Blue Stream and Turkish Stream pipelines. On March 17-19, 26 Ukrainian UAVs attacked Russkaya and Kazachya compressor stations of Blue Stream gas pipeline and Beregovaya compressor station of Turkish Stream gas pipeline. The attacks were repelled. Total capacity of the gas pipelines is 47.5 BCMA (130 mcm/d). If future attacks are successful, Turkey may face sudden energy crisis. Summer season is a low-demand period in Turkish market. Peak is reached during cold months of winter. This reduces the relevance of current global gas crisis for Türkiye.

QatarEnergy reported destruction as a result of the attack of two of its fourteen LNG trains, with a combined capacity of 12.5 MTPA. The trains were co-owned by ExxonMobil (USA).

China, India, and Pakistan are the largest buyers of Qatari LNG. It is Asia that has been key victim of provocative Israeli attack.

In 2025, Qatar became the leading supplier of LNG to China.

Now China will be forced to increase its purchases of Australian LNG. There is a chance that Chinese state-owned companies will open their terminals for Russian LNG from Arctic LNG 2 and Baltic medium-tonnage projects. Similar discussions are taking place in oil market regarding admission of Russian "sanctioned" oil to crude import terminals of Chinese state-owned oil companies.

Qatar provided 100% of LNG imports to Pakistan. At the same time, Pakistan faced the problem of excess supplies due to stagantion of domestic gas market. In recent years, Pakistan has cancel a lot of Qatari LNG cargoes due to oversupply even under pre-war price levels. Now the problem is the opposite - Pakistan is forced to find all the necessary import volume on spot (!) market. This creates crisis conditions for poor Pakistani gas market.

Qatar has been a leading supplier of LNG to India. UAE, which also are off the market, is the second leading supplier.

LNG itself accounts for half of India's gas market (the rest is locally produced gas). India's energy system is predominantly coal-based and can withstand reduced gas supplies. However, simultaneous market crisis in LNG, LPG, and oil supplies, coupled with rising energy import prices, places immense pressure on India's financial system. Rupee's exchange rate is currently being artificially maintained through burning of Indian gold and foreign currency reserves. Prolonged war in Middle East will inevitably lead to a weakening of rupee and further increases in energy import prices denominated in rupees. All of this leads to a collapse in domestic gas demand, primarily aming domestic fertilizer producers.

USA is absolute winner from the strikes. They will take advantage of not only the extremely high LNG prices, but also the freed-up space for new LNG projects that are now being launched - 26.7 MPTA of new capacity will be commissioned in 2026.

Whatever Trump says, this Israeli blow has brought a lot of money to the US.

Russian LNG projects, which have been blacklisted by the West, may reimprove their position in international LNG market. However, this is levered by lengthening of LNG export logistics routes from the Baltic and Yamal regions due to seasonal freeze of Arctic ocean and Ukrainian attack on Russian LNG carrier in Mediterranean Sea, caused by a shortage of available LNG carriers of both ice-class and non-ice-class. However, the situation will improve significantly with opening of summer navigation on Northern Sea Route.

Notes:

Join Seala AI’s Linkedin page to be informed for all new future releases with new dashboards and insights.

Non-mainstream oil and gas news and views are available in Seala AI’s telegram channel.

Full set of reports for each country and much more information are available via Seala AI terminal.