Gas industry of Qatar

Summary

History of Qatari gas industry begins with discovery of super-giant North field in 1971 and establishment of Qatar Fuel (now QatarEnergy LNG) in 1984 to develop it in collaboration with Western technology and financial partners. The first LNG cargo was shipped in 1996.

Qatar ranks third in the world in terms of gas reserves, after Russia and Iran. The key asset is North field (Qatari part) / South Pars field (Iranian part), which is jointly developed with Iran.

As of March 2026 technically-operational LNG production capacities is estimated at 64.6 MTPA. These capacities are currently idle due to Israeli-US war against Iran.

In 2027-2028 QatarEnergy LNG plans to commission 47 MTPA of new LNG liquefaction capacity.

In 2010, Qatar became the leading LNG exporter to the global market for the first time. In 2025, Qatar became the second-largest LNG exporter to the global market, with an export volume of 84.7 million tons (utilization of the plant’s design capacity - 110%). Due to the ongoing war between Israel and USA against Iran, Qatari LNG production and exports are expected to decrease significantly in 2026. As of March 2026, production has been almost completely halted, and exports have ceased.

Top countries importing Qatari LNG are China (including Taiwan), India and Pakistan.

Qatar has the largest in the world gas-to-liquid plant Pearl GTL. The plant is owned by Shell and has project capacity 16.5 bcm per year.

Qatar exports gas via pipeline as well. Importers of Qatari pipe gas are UAE and Oman. Export volume is up to 20 bcm per year.

QatarEnergy LNG is key company in Qatari gas market. QatarEnergy has made the Al Thani family, the rulers of Qatar, the richest people on the planet.

Map of gas industry

Reserves

Qatar ranks third in the world in terms of gas reserves after Russia and Iran.

Key asset is North field (Qatari part) / South Pars (Iranian part) joint field with Iran.

The second major gas field in Qatar is Dukhan.

LNG and gas processing plants

Ras Laffan plant

The plant is controlled by QatarEnergy LNG and has many minority shareholders of each train.

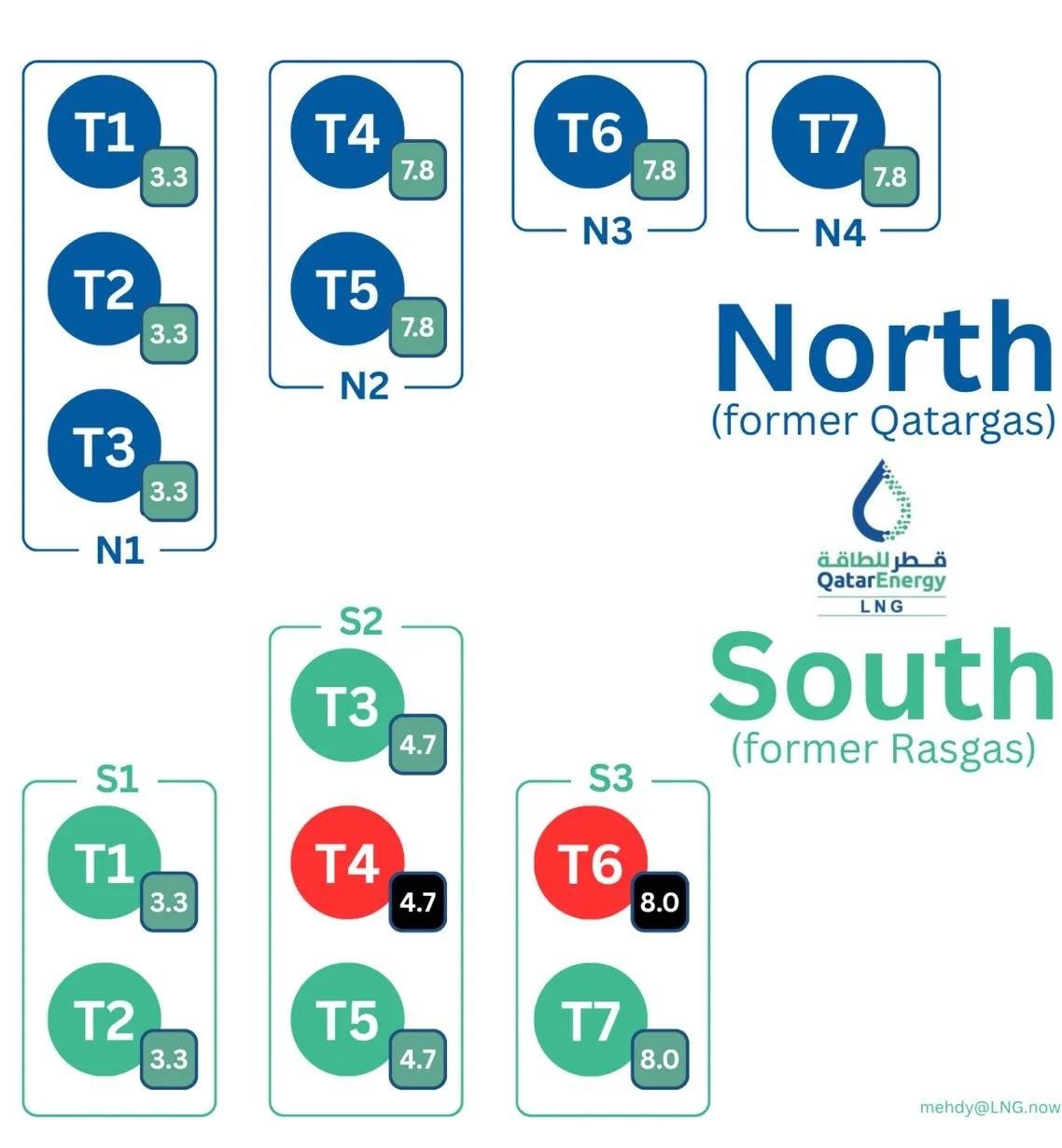

Recently two LNG plants of Qatar (QatarGas and RasGas) were reorganized in one mega plant, the biggest on Earth, with combined capacity 77 MTPA. As aftermath of Iranian retaliation strikes two trains with combined capacity 12.5 MTPA were heavily damaged and will not produce LNG for year. Remaining capacity is 64.6 MTPA.

Qatar is on the way to build new 47 MTPA capacities of new LNG trains of its two plants. These capacity additions are scheduled to go live 2027-2028.

The plant produce helium. Helium production is a part of the technological chain and is separated into Helium plant. The helium plant consists of three lines with total capacity of 67 mcm per year (95 million liters of liquid helium per year). The first line was launched in 2014, and the last line was launched in 2021.

Pearl GTL plant

The plant is 100% controlled by British company Shell. At the same time, Shell and QatarEnergy have an production sharing agreement for all processing at this plant.

Feed gas for processing comes directly from 22 offshore wells in Persina gulf.

Capacity of the plant is 16.5 bcm per year (45 mcm per day). As a result of Iranian retaliatory strikes in March 2026, the plant's operating capacity was reduced by half.

The plant produces naphtha, kerosene, base oils, and NGL (ethane and others).

LNG export

LNG loadings

The table “Monthly LNG loadings volumes “ provides statistics on the loading of gas carriers at Ras Lafan, the only LNG loading port in Qatar. The data is available from October 2022. 01.MM.YYYY means shipments for the entire calendar month starting on that day. Shipments for the current month are indicated by cumulative total from the first day of the month to the current date. The delay in receiving data is up to one day. The data is updated automatically.

The table “Details of LNG loadings in Qatar during last 30 days“ provides the data on loading of gas carriers at gas-liquefying plants ar Ras Laffan during last 30 days and is updated automatically.

LNG export destinations

The table “Destination countries of Qatari LNG Export" provides statistics on importing countries of Qatari LNG with aggregation by calendar months. The date of gas carrier loading is used, the data on importing country is available upon discharge. The data has been provided since 01.09.2022 and is updated automatically. Data for the current month is shown as a cumulative total.

Current top importers of Qatari LNG are China (including Taiwan), India and Pakistan.

China

In 2025 Qatar became number one supplier of LNG to China.

India

For India, Qatar is the number one LNG supplier.

Pakistan

In September 2025, Pakistani LNG importers Pakistan State Oil Company (PSO) and Sui Northern Gas Pipelines Limited (SNGPL) requested QatarEnergy’s consent to reduce the number of cargoes under existing SPA. These companies presented the Qatari exporter four options for rationalizing LNG supplies due to limited flexibility under existing contracts. This step was taken due to t oversupply of regasified liquefied natural gas at domestic marker caused by a decrease in demand from private and energy consumers. A decrease in demand, especially from gas TPPs, after an increase in fixed tariffs and the introduction of autonomous fees, led to a surplus of natural gas on the market. It is predicted that between July 2025 and 2031, about 177 LNG cargoes will remain surplus.

In October 2025, it was reported that Pakistan plans to cancel 24 shipments of LNG from Qatar in 2026.

EU

Qatar is the number three LNG supplier to EU. Top EU receivers are Italy, Belgium, Poland and Span.

Qatar is consistently increasing its penetration into the European gas market, including long-term lease of regasification terminals. QatarEnergy aims at control of supply chain from natural gas well to wholesale gas markets sales in North-Western Europe.

In Q4 2024 European Commission due to Qatar's non-subordination to Europe (the official wording, as always in Europe, is different - due to “non-compliance with environmental norms and social standards”) announced an additional tax (formally in the form of a fine) on LNG imports from Qatar in the amount of 5% of global revenue Qatar Energy. The estimated amount of the payment requested by the EU for the right to continue supplying Qatari gas to the block is 8 bAED / 16 bCNY / 181 bINR / 210 bRUR / 2 bUSD. In October 2025, Qatar's Minister of State for Energy and CEO of Qatar Energy Saad bin Sharida al-Kaabi explicitly indicated that Qatar is considering refusing to supply LNG to EU if an attempt was made to confiscate amount of the so-called fine.

UK

In July 2025, QatarEnergy began deliveries to Isle of Grain regasification terminal near London area under 25-year lease agreement for 7.2 MTPA of regasification capacity (half of the terminal's total capacity). This indicates Qatar's desire to maintain supplies to the European market and reduce dependence on the decisions of European Commission.

Shippers of Qatari LNG

Qatari state-owned shipping company Nakilat is the main carrier of Qatari LNG. The company has both its own LNG fleet and a number of joint ventures with foreign shipping and energy companies. These joint ventures (with the exception of Maran Nakilat) are 100% focused on transporting Qatari LNG.

Qatar is currently the world's largest customer for new LNG carriers. These carriers are needed to support the upcoming expansion of the LNG plant.

Pipeline export

UAE and Oman

Qatar-based Dolphin Energy produces gas at North Field, processes at the Gas Processing Plant in Ras Laffan Industrial City, and then transports the gas by offshore pipeline to Gas Receiving Facilities at Taweelah in Abu Dhabi, UAE and further to Oman. The facility has started gas supply in July 2007. Capacity is significant 57 mcm per day.

Abu Dhabi state fund Mubadala owns 51% share of the company. The other 49% owned by French TotalEnergies and US Oxy.

Domestic market

Gas-fired power generation

Installed capacity of gas-fired TPPs in the country is 12.6 GW. Theoretical maximum demand from gas generation is 76 mcm/d.

Production and export of helium

Helium is produced at the LNG plant as part of the purification process of extracted natural gas. Export takes place in ISO containers with liquid helium.

Qatar exports the entire volume of helium produced.

In 2017, QatarEnergy interrupted production and export of helium at the RasGas plant due to tense trade relations in the region.

Volume of helium production in Qatar in 2023-2025 was 63-65 mcm of helium per year. This corresponds to almost 100% of design capacity of the helium plant and 35% share in global production.

In 2025, Qatar became the world's leading exporter of helium with a volume of 63.5 mcm of helium and market share of 48%. Helium supplies are mainly carried out under long-term contracts. Main consumers of Qatari helium are Asian countries (41 mcm, 64.4%), including China (15 mcm), EU and UK (30%), and USA (3.5%).

Impacts of wars

War of Israel and USA against Iran

Qatar participated in Israeli-US attack on Iran in 2026. As a result of the retaliatory strikes, oil and gas facilities in Qatar were damaged:

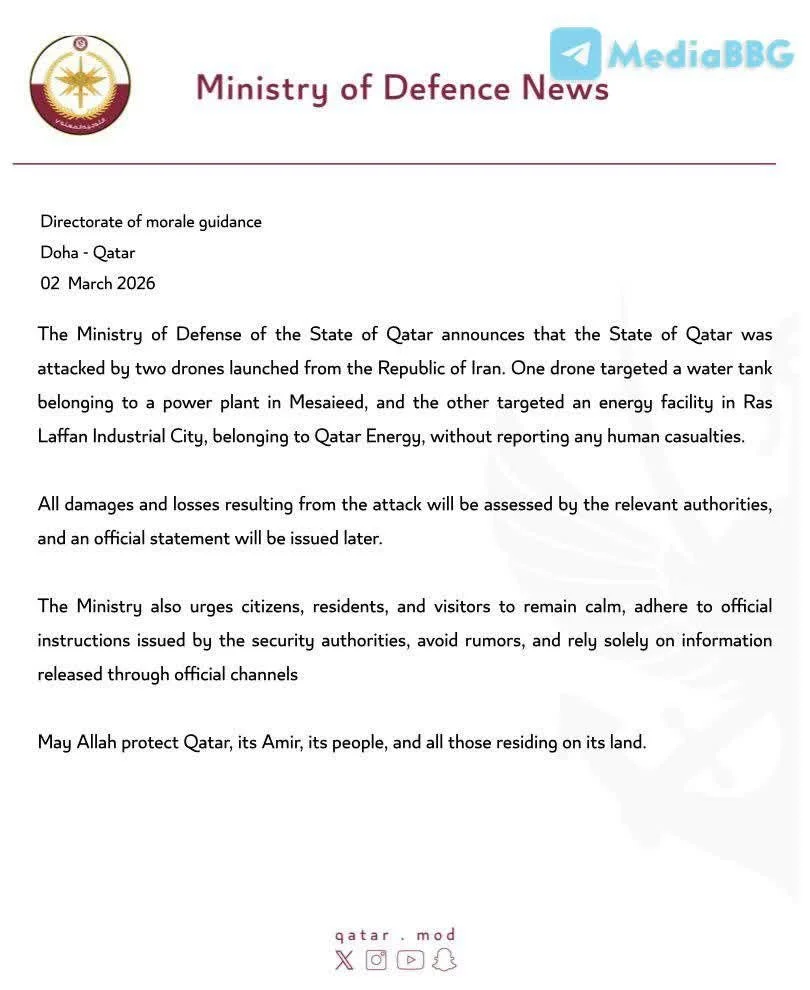

02.03.2026 - LNG plant in Ras Laffan was hit. QatarEnergy LNG shut down the plant and declared a force majeure event regarding its obligations to load LNG.

Official statement

18.03.2026 - strikes to Pearl GTL. It is reported that one of two trains were heavily damaged.

18-19.03.2026 - Iranian retaliation strikes heavily damaged Ras Laffan LNG plant. QatarEnergy reported destruction as a result of the attack of two of its fourteen LNG trains, with a combined capacity of 12.5 MTPA. The trains were co-owned by ExxonMobil (USA).

06.07.2026 - Qatari gas carrier Al Rekayyat (9397339) was attacked while attempting to pass through Strait of Hormuz through Omani part without Iran's approval.

As of end of March Qatar has the following consequences of the war:

Qatar will need at least two weeks after end of the war to restore production at remaining 64.6 MTPA capacity of Ras Laffan.

12.5 MTPA of Ras Laffan capacity are heavily damaged and should be rebuild, which will require 3-5 years. Although there are 46.8 MTPA capacities of under construction, which scheduled to be delivered in 2027-2028. It will make up any decrease in Qatari production in mid-term.

Scheme of trains at Qatari LNG

Qatari 2026 GDP will shrink at least for 4% for each month of Strait of Hormuz closure.

Notes:

Join Seala AI’s Linkedin page to be informed for all new future releases with new dashboards and insights.

Non-mainstream oil and gas news and views are available in Seala AI’s telegram channel.

Full set of reports for each country and much more information are available via Seala AI terminal.