LNG market in Q1 2026

Summary of events in Q1 2026

Israel's March 18 attack on Iran's South Pars gas field and Iran's retaliatory strikes on Qatar's Ras Laffan LNG plant, which liquefies gas from the North Field, have significantly reduced physical availability of gas in Asian region and caused an increase in prices for LNG supplies under spot contracts with a pricing linked to gas hubs and long-term contacts with a pricing linked to average crude oil prices. On 08.04.2026, a temporary truce was declared. It is reasonable to expect resume of military attacks within a year. On 12.04.2026 USA joined to the blockade of the Strait of Hormuz from outer side.

Attack by Ukraine, Great Britain and Libya on Russian LNG carrier Arctic Metagaz and low availability of ice and non-ice class LNG carriers for Russian exporters limit possibilities of Russian LNG exports, especially during the first half of a year.

As of 08.04.2026, there were 49 LNG plants in the world with total LNG liquefaction capacity of 446 MTPA. Q-o-Q decrease - 71 MTPA. 10 plants were fully or partially idle with total non-operational capacity of 100 MTPA, including united LNG plant in Qatar and Das Island LNG in UAE.

Start of operations at Barossa gas field in Australia on 28.01.2026 allowed to restart Darwin LNG (3.7 MTPA), which was idle since November 2023.

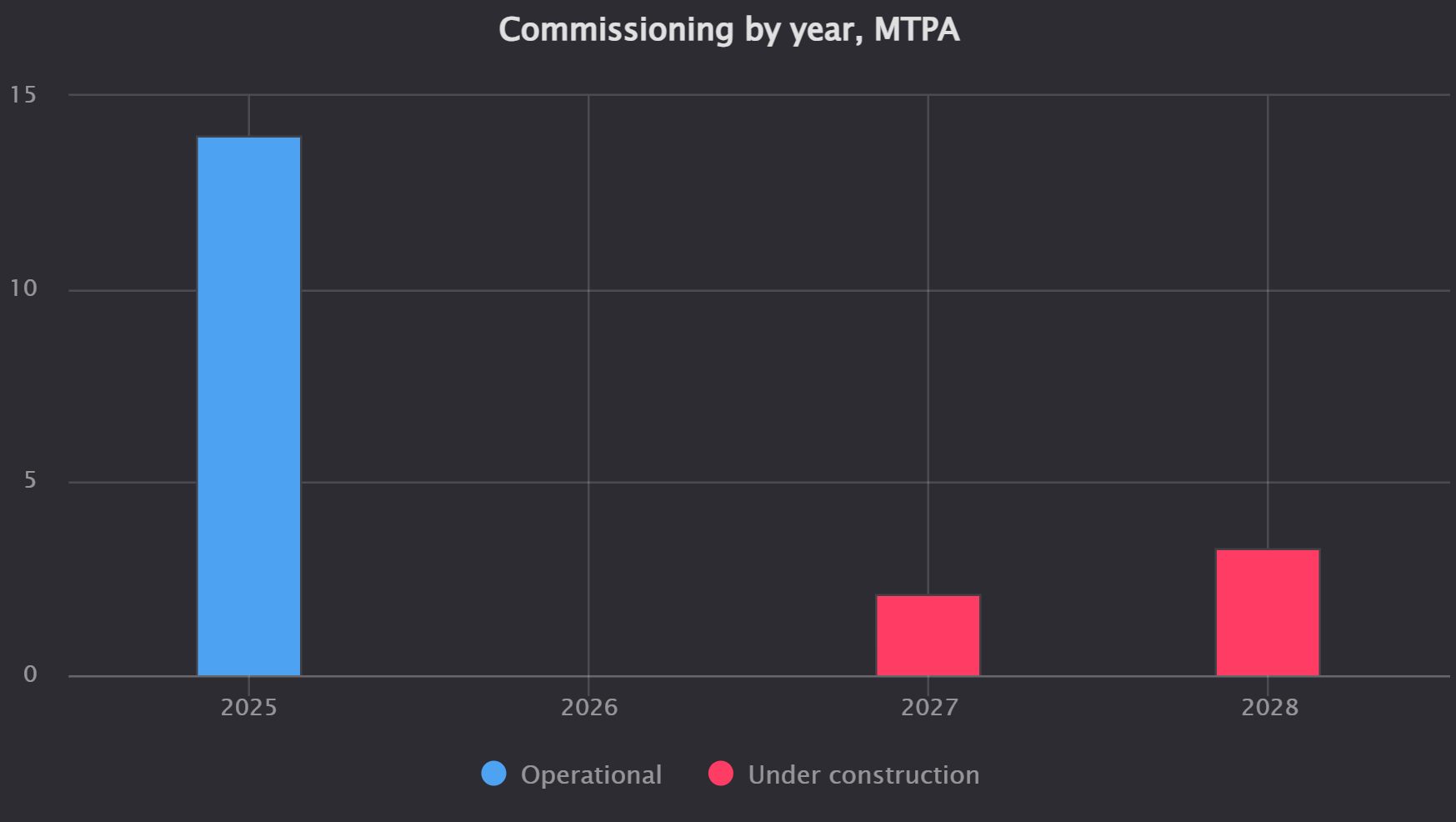

In 2026, 41 MTPA of LNG capacity is expected to be commissioned. USA dominates this process - it will account for 65% in 2026. War in Middle East will delay Qatari and Emirati newbuilds.

USA remained to be number one supplier of LNG to the global market in Q1 2026. Australia is the second. Qatar has almost stopped LNG production in March, but good January and February results helped to finish Q1 as Top-3 LNG supplier. Russia is the fourth. Canada keeps rising in the ranking.

As of 08.04.2026, there were 206 regasification terminals in the world with total regasification capacity of 1099 MTPA.

Regasification capacities of 98 MTPA are expected to be commissioned this year. Y-o-Y growth is 9%. China’s share in capacity build up is 36%. Egypt and India are in top 3.

Japan regained the title of the main importer of LNG in the world as result of Q1. The key reason is decline of Chinese LNG import by 27% (5.1 million tons). South Korea is the third with a slight lag behind China. India reduced LNG imports and took only the sixth place in the ranking of importers.

On 03.12.2025, European Council and European Parliament decided to abandon import of Russian gas into EU. Pipeline gas supplies must stop no later than 30.09.2027, and in some cases before 01.11.2027. A transition period is provided for existing contracts. For short-term contracts signed before 17.06.2025, the ban will take effect from 25.04.2026 for LNG and from 17.06.2026 for pipeline gas.

As of 07.04.2026, remaining stocks of active natural gas in UGS of EU and UK amounted to 32.1 bcm. Stocks are significantly lower than in previous years – minus 6.7 bcm compared to previous year and minus 33.3 bcm compared to 2024. It is second lowest volume after 2022.

As of 07.04.2026, there were 819 operational linear LNG carriers with 58.3 MT of total cargo hold capacity. LNG carriers with 7.5 MT of total cargo hold capacity are expected to be commissioned in 2026. It will be all-time high value. Expected Y-o-Y increase is 21%.

Due to decrease in natural gas production in Persian Gulf region and the blockade of the Strait of Hormuz, export of by products, primarily LPG and helium, has also suffered. Given significant share of the region's countries in global supply, this has led to shortages and market price growth.

LNG plants

As of 08.04.2026, there were 49 LNG plants in the world, including partially idle ones, with a total operational LNG liquefaction capacity of 446 MTPA. Q-o-Q decrease - 71 MTPA.

10 plants were completely or partially idle with a total non-functioning capacity of 100 MTPA. List of idle plants and trains:

All but one trains of Qatari LNG plants. Two trains of the plant are considered to be destroyed.

Adgas Das Island in UAE. Presumably complex keeps extracting and treating natural gas and supply it to UAE shore via undersea gas pipeline.

Marsa el Brega LNG in Libya.

Yemen LNG.

Train 1 at the Atlantic LNG plant in Trinidad and Tobago.

Cryogaz-Vysotsk plant in Russia

Trains C, D, E of the Botang LNG plant in Indonesia.

Train 2 of the Northwest Shelf LNG plant in Australia.

Damietta LNG plant and Egyptian LNG plants in Egypt. EGAS at Idku discharges rare LNG cargoes from time to time.

As of 08.04.2026 trains at 23 plants (including expansion projects for existing plants and debottlenecking projects) are under construction with new liquefaction capacity of 189 MTPA . Such an extremely high development rate for any industry indicates the upcoming changes in the industry in the coming years, which will be negative for LNG producers.

In 2026, 41 MTPA of LNG capacity is expected to be commissioned. USA dominates this process - it will account for 65% in 2026.

It is highly likely that starting in summer of 2028, LNG will be in relative proficity, which will lead to lower prices. This market conditions will lead USA of clearing again global LNG market from countries they dislike - Russia, Iran (cross-border pipeline gas trade). US attention to Qatar is also likely to increase.

Loading

According to Seala AI, USA remained to be number one supplier of LNG to the global market in Q1 2026. Australia is the second. Qatar has almost stopped LNG production in March, but good January and February results helped to finish Q1 as Top-3 LNG supplier. Russia is the fourth. Canada keeps rising in the ranking.

USA

Q1 LNG shipments from USA amounted to 32.4 million tons. Utilization of existing by the end of the quarter capacities exceeds 100%.

USA continues to successfully monetize the crisis in Eastern Europe started in 2013 under Biden administration (vice president in 2009-2017, president in 2021-2025) and consequent elimination of Russian energy resources from the European market. Commissioning of US LNG plants is synchronized with the disconnections of Europe from Russian gas and LNG. In the coming years, balancing of West of Suez gas market will be done y USA by limitation of export of Russian pipeline gas and LNG.

Integrared gas market of EU and UK is dominant buyer of Q1 US LNG.

Türkiye has become the second largest buyer of Q1 US LNG with 2.5 million tons. Türkiye traditionally buys majority of its LNG during heating season. The total volume of purchases is growing every season.On 09.01.2026 Australian Woodside and BOTAŞ have signed a long-term agreement to supply LNG to Turkish market. Under the contract, Woodside Energy will supply BOTAŞ approximately 500 kt annually for up to nine years, beginning in 2030. LNG will come primarily from Louisiana LNG project in USA, as well as from other Woodside assets.

Egypt became the third largest buyer of Q1 US LNG resource with 2.3 million tons.

USA supplied 1.1 million tons in Q1 to Caribbean countries (Panama, Dominican Republic, Jamaica, Colombia) excluding Puerto Rico.

Details of LNG shipment from the USA are available at the link.

Canada

Q1 LNG shipments from Canada amounted to 2.5 million tons.

Canada LNG is on the way to overcome technical difficulties affecting its core operations. In Q1 it is still not performing on the level of design capacity (1167 kt per month).

Q1 cargoes were delivered to East Asia and South-East Asia. Key buyers are South Korea, Japan and China (including Taiwan province).

Two more local LNG plants are underway:

Woodfibre LNG plant near Vancouver with capacity of 2.1 MTPA.

Cedar FLNG plant next to Canada LNG with capacity of 3.3 MTPA.

Canada LNG capacity build-up

Mexico

Q1 loadings volumes amounted to 278 kt.

Construction of LNG facilities is under way in Mexico - as of 20.04.2026 - 4.7 MTPA capacity is under construction and 25.8 MTPA is planned.

Construction projects (Energia Costa Azul LNG, New Fortress Altamira FLNG) are delayed again. Сurrent estimate of launch date for Energia Costa Azul LNG is summer 2026. US Department of Energy has extended permit for export of pipeline gas from USA to Mexico to this plant until the end of September 2026. The previous permit expired at the end of March.

Сompletion of construction work on the second 1.4 MTPA train of New Fortress Altamira FLNG is expected to be completed in Q4 2026 and commercial operations are expected to begin in H1 2027.

Construction of Amigo LNG plant with a total capacity of 8.4 million tons per year will start soon.

Trinidad and Tobago

Q1 2025 LNG loadings amounted to 1.9 million tons. Utilization of operational capacities of the only LNG plant Atlantic LNG (11.8 MTPA without idle Train 1) - 65%.

Traditionally, LNG from Trinidad and Tobago is shipped worldwide and has a diversified customer base.

Peru

01.03.2026 an major accident occurred at the largest gas field in Peru. As a result, LNG production was halted.

Ministry of Energy and Mining Industry estimates consequences of the accident as the largest energy crisis for the country in 20 years. A 14-day state of emergency has been declared in Peru. Availability of gas for domestic market has decreased by 10 times.

As a result of the accident, LNG supplies from Peru in Q1 decreased and amounted to 692 kt.

Qatar

Qatar participated in attack of Israeli and US on Iran.

02.03.2026 Iran struck Ras Laffan LNG plant first time. QatarEnergy shut down Ras Laffan plant to limit potential future damage and declared a force majeure event regarding its obligations to load LNG.

18-19.03.2026 as a retaliation strike to Israeli and US strike to Iran's South Pars gas field Iran striked twice to Qatar's Ras Laffan LNG plant. Qatar reported destruction two of its fourteen LNG trains, with a combined capacity of 12.5 MTPA. The trains were co-owned by ExxonMobil (USA).

March loadings at Ras Laffan shrinked near to zero. And almost all loaded in March cargoes are locked in Persian Gulf as of 09.04.2026.

It is Asia that has been key victim of provocative Israeli attack. China, India, and Pakistan are the largest buyers of Qatari LNG.

As of end of March Qatar has the following consequences of the war:

Qatar will need at least two weeks after end of the war to restore production at remaining 64.6 MTPA capacity of Ras Laffan.

12.5 MTPA of Ras Laffan capacity are heavily damaged and should be rebuild, which will require 3-5 years. Although there are 46.8 MTPA capacities of under construction, which scheduled to be delivered in 2027-2028. It will make up any decrease in Qatari production in mid-term.

Annual Qatari 2026 GDP will shrink at least for 4% for each month of Strait of Hormuz closure.

In scenario of a prolonged halt in military operations in the Gulf and the continued blockade of the Strait of Hormuz, QatarEnergy may restart some of its LNG trains to meet demand for LNG within Persian Gulf. From May to September, demand for electricity and natural gas for its production peaks in Middle East. This will allow restart of several trains at the plant (up to 25% of its capacity).

Details of Qatar's exports are available at the link.

UAE

UAE participated in attack of Israeli and US on Iran. As a result of retaliation strikes 7.6 MTPA Adgas Das Islang LNG plant were shut down early March to avoid possible explosions.

Q1 LNG production amounted to 1.1 million tons.

The second LNG plant in the country, Ruwais, is expected to be launched in 2029. The plant's capacity will be 9.6 MTPA.

Discharge at regasification terminals in Jebel Ali and Abu Dhabi amounted to 147 kt in Q1. Cargos came from Qatar, UAE. Traditionally, discharges at this terminal peak in Q3 of each year during heat wave.

Details of Emirati gas market are available here.

Oman

Oman's only LNG plant Qalhat is located on the shores of the Gulf of Oman. The closure of the Strait of Hormuz did not affect shipments from this plant.

LNG loading volumes in Q1 amounted to 3.0 million tons. Plant’s utilization - 107%. Majority of Q1 cargoes went to India, Japan, China, Taiwan and South Korea. March LNG cargoes from Oman to India was at the highest of all time of observation - India is desperately replacing Qatari LNG.

In January Omani Asyad Shipping sold to Russian Novatek-related entity 4 LNG non-ice carriers.

Iran

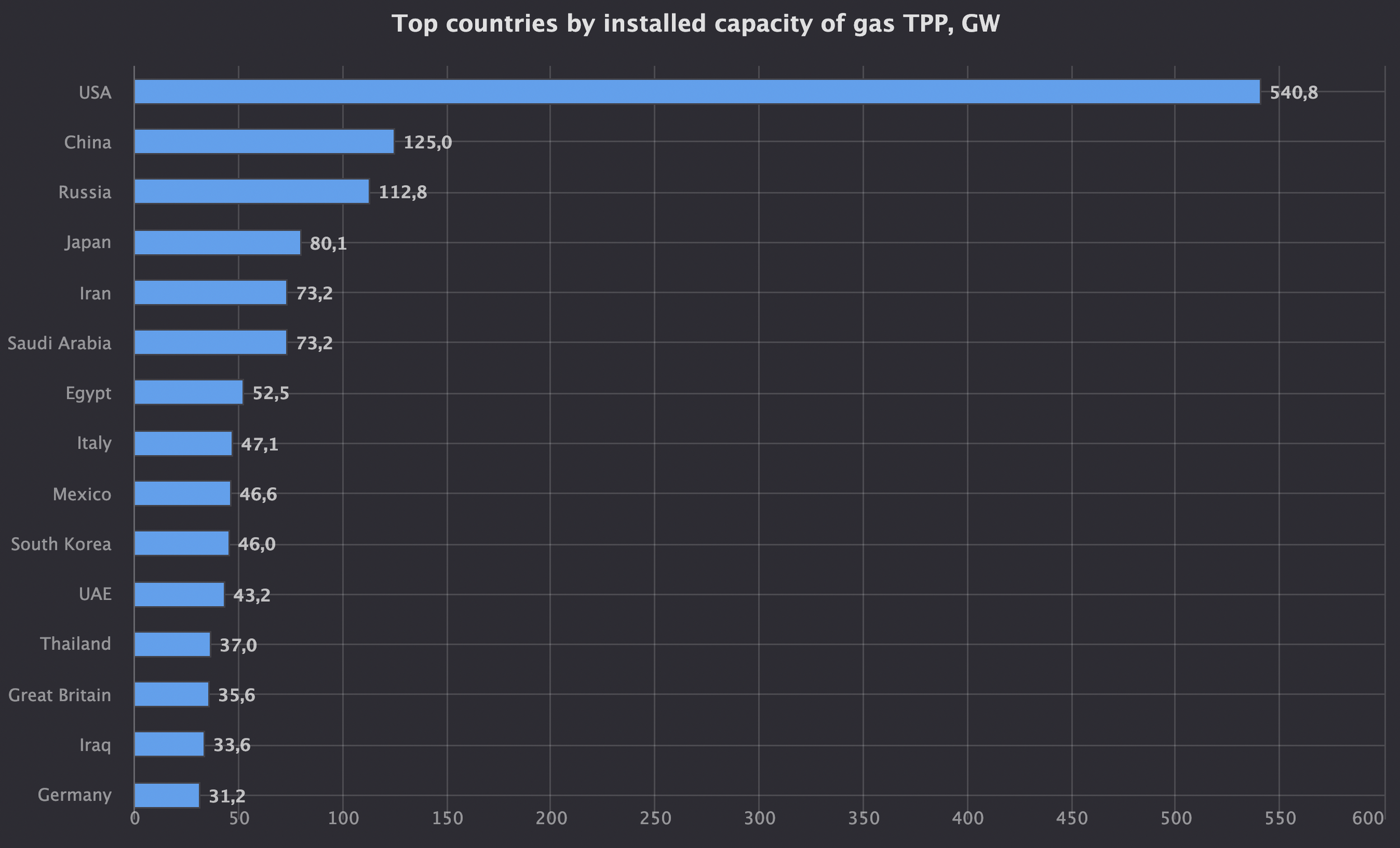

As a result of the Israeli attack Iranian domestic gas and electricity consumers has suffered. Iran's domestic market is the fourth-largest in the world, after USA, China, and Russia - 265 billion cubic meters per year (BCMA). South Pars accounted for 70% of Iran's gas production (716 mcm/d as of June 2025). As of now there is no information what is remaining production rate and what will be recovery period.

Iran is one of the leaders in gas generation. Installed capacity of gas-fired TPPs in the country is 73.2 GW. Theoretical maximum demand from gas generation is 440 mcm/d. Gas-fired TPPs provides 86% of the country's electricity generation mix. So sharp decrease in gas supply will have immediate effect on domestic power supply.

Iran has also stopped exporting pipeline gas to neighboring Iraq. At the same time, export of pipeline gas to Türkiye remained.

Details of Iranian gas market are available here.

Australia

Gas production developments and LNG plants update

In December 2025 stage 2 of development of Waitsia gas field was launched. It provided additional gas resources for Northwest Shelf LNG plant.

Barosso gas field was launched in Q1.

Start of operations at Barossa gas field in Australia on 28.01.2026 allowed to restart DarwinLNG plant (3.7 MTPA). The plant had been idle since November 2023.

Scarborough natural gas field, located in Carnarvon Basin, about 375 km off the coast of Western Australia, is expected to be commissioned in Q4 2026. The development includes the installation of a semi-submersible floating production facility moored at a depth of 950 m, connected by a pipeline with a length of about 430 km to the second train of Pluto LNG plant with 5 MTPA capacity at an existing onshore facility.

In December 2025, Australian government made a proposal to reserve from 15 to 25% of gas produced for domestic market starting in 2027. Presumably, this will affect the possibility of concluding new LNG supply contracts in 2027 and later.

LNG loadings

Q1 LNG loadings at Australian plants amounted to 20.8 million tons.

In Q1 2025 Australia traditionally became the number one LNG supplier to Japan and South Korea and regain number one in China.

Details of Australia's exports are available at the link.

Papua New Guinea

Q1 2026 loadings at the country's only LNG plant (8.3 MTPA) quarter amounted to 2.0 million tons. Utilization of the design capacity was 96%.

All cargoes went to neighboring East Asian countries - Japan, China (including Taiwan) and South Korea.

Brunei

Q1 2026 loadings at the only LNG plant (7.2 MTPA) amounted to 1.6 million ton. Utilization of the design capacity was 91%.

All Q1 cargoes went to neighboring East Asian countries - Japan, Taiwan, South Korea and others.

Indonesia

Loadings at Indonesian LNG plants amounted to 4.7 million tons in Q1.

Discharge of domestic Q1 LNG at own regasification terminals amounted to 1.3 million tons (27% of the country's production).

South Korea, Japan and China (including Taiwan) are key external consumers of Indonesian LNG.

Malaysia

Q1 LNG loadings at Malaysian plants amounted to 7.9 million tons. Utilization of the design capacity (32 MTPA) was 98%.

Deliveries of Malaysian LNG to domestic regas terminals amounted to 369 kt (5% of domestic LNG production).

LNG discharges at two Malaysian regas terminals (Pengerang LNG, Melaka FSRU) amounted to 1.3 million tons in Q1. Australia is the leading supplier.

Details of Malaysia's exports are available at the link.

Russia

In Q1 Ukraine continues to attack Russian gas supplies to the global gas market:

03.03.2026 - Ukrainian unmanned boats destroyed Russian gas carrier Arctic Metagaz (9243148) off the coast of Libya. Unmanned boats were launched from the coast of western Libya.

17-19.03.2026 - Ukrainian UAVs attacked Russkaya and Kazachya compressor stations of Blue Stream gas pipeline and Beregovaya compressor station of Turkish Stream gas pipeline from Russia to Türkiye. The attacks were repelled.

02.04.2026 - Ukrainian UAVs attacked Russkaya compressor stations of Blue Stream gas pipeline. The attack was repelled.

05.04.2026 - Attempt of Ukrainian agents to blow up gas pipeline between Hungary and Serbia, which is a continuation of Turkish Stream. The attack was prevented.

If the next waves of similar attacks lead to damage of gas infrastructure, exports of Russian pipeline gas and LNG could be severely affected. Pipeline exports will be irretrievably lost, and LNG carriers with Russian cargoes will have to sail around Africa via the Cape of Good Hope, which will not only reduce marginality of the export, but also reduce its volume due to shortage of LNG carriers available to Russian exporters.

LNG plants loadings

Q1 LNG loading at the plants amounted to 9.3 million tons. On top of it 1.3 million tons were loaded on transhipment hubs (mostly at Kildin island STS zone and floating storage Saam).

5.3 million tons were shipped from Yamal LNG (Sabetta port).

2.9 million tons was loaded at Sakhalin-2 (Prigorodnoye port) at par with Q4. Most of Q4 cargoes went to Japan. Japan continues to receive so-called “permits” from the United States to import LNG from Sakhalin-2. There were also shipments to China and South Korea.

Per Seala AI data, Arctic LNG 2 Q1 loading 848 kt. Shortage of Arc7 ice-class LNG carriers has reduced ability to export LNG from Arctic LNG 2 in cold times.

LNG carriers with Arc7 ice-class are required to export LNG from Arctic LNG 2 in December - May. In December 2025 - January 2026, only one such LNG carrier, Christophe de Margerie (9737187), operated in shuttle mode between Utrenny terminal (Arctic LNG-2) and Saam FSU (9915090) in Murmansk oblast. In January 2026, new Russian Arc7 ice-class LNG carrier Alexey Kosygin (9904546) has joined this route. It doubled the ability to export and, consequently, produce LNG to Arctic LNG 2.

As a measure to increase the fleet of non-ice-class LNG carriers, purchases of LNG carriers continue on secondary market. In January, 4 LNG carriers (Mercuriy - 9326689, Kosmos - 9300817, Orion - 9294264 and Luch - 9317315) were purchased from Omani company Asiad Shipping, and since the beginning of April, they have been flying Russian flag. These vessels will likely load LNG from Saam and Koryak floating storages and deliver it to final buyers in China and other countries.

Another challenge is the lack of regas terminals (except for Beihai) to reach the design capacity of both 6 MTPA trains of the plant.

Medium-tonnage plant Gazprom LNG Portovaya kept working in Q1.

Cryogaz-Vysotsk has been idle in Q1.

Transit to Kaliningrad region via Lithuania

Since 01.01.2026 renewed 5 years agreement on transit of Russian gas through Lithuania to Kaliningrad Region took into effect. Transit price increased 2.2 times to 29 million euros / 2.7 billion rubles. Unit cost of transit will increase to 0.05 AED / 0.10 CNY / 1.02 INR / 1.07 RUR / 1.35 US.

It helps to free related Russian LNG infrastructure for export of LNG from Gazprom LNG Portovaya instead of supplying Kaliningrad oblast.

Details of Russian gas market are available at the link.

Norway

Q1 2026 loadings at the country's only large-tonnage plant Hammerfest Snøhvit (4.2 MTPA) amounted to 1251 kt. Achieved utilization was 119%. All cargoes went to EU and UK. Lithuania was the biggest buyer of Q1 cargoes.

Small-scale Risivika (330 kt per yer) operated at its design capacity and provided LNG bunkering and small parcels for local consumers.

Mozambique

Q1 2026 loadings at the only LNG plant Coral South (3.4 MTPA) amounted to 883 kt. This indicates 104% utilization of the plant.

LNG from Mozambique is supplied to wide list of countries. Asian countries dominate among the recipients.

Western energy companies keeps developing new LNG projects in Mozambique.

The country's second Coral North floating LNG plant with a planned capacity of 3.4 MTPA is expected to be commissioned at the end of 2027. Owners of both Coral projects are Italian Eni, US ExxonMobil, Chinese CNPC, Korean Gas Corporation of South Korea, UAE’s ADNOC and local Empresa Nacional Hydrocarbons. Mozambique's share in these projects is 10%. LNG sales of ENH’s 10% share are controlled exclusively by Dutch Vitol.

French TotalEnergies keeps development of Mozambique LNG Zone 1, onshore project with 13 MTPA capacity, after lifting force majeure in October 2025. Meanwhile TotalEnergies demands compensation from Government of Mozambique in the amount of 4.5 billion USD for the delay in the implementation of the project.

ExxonMobil’s Rovuma LNG (18 MTPA) project is under development as well. Final investment decision is expected in 2026.

Thus potential Mozambique’s liquefaction capacity is up to 38 MTPA. It could make Mozambique one of the leader of LNG industry.

Details of Mozambique's LNG industry are available at the link.

Angola

LNG exports from Angola amounted to 1155 kt in Q1. The plant’s utilization - 89%. Supplies are stable.

India consumed more than half of Q1 resource.

Previously, Angola LNG's main resource was associated gas from offshore oil platforms.

Increase in gas production at depleted Sankha oil field has provided 2.3 mcm per day (0.8 bcm per year) of additional resource for Angola LNG in 2025. At the second stage of production improvement at this field, additional supplies to the LNG plant are expected in the amount of 6 mcm per day (2.2 bcm per year).

Natural decline in oil production led to a decrease in the associated gas resource for the LNG plant. New gas consortium plans to add up to 12 mcm of gas for the LNG plant from the second stage of Quiluma and Maboqueiro gas fields, which will ensure full utilization of the plant and give feasibility for its expansion.

Republic of the Congo

There are two FLNG in the country: 0.6 MTPA Tango FLNG and 2.4 Nguya FLNG. Plants are owned by Italian ENI (65%), Russian Lukoil (25%) and domestic SNPC (10%) with production sharing approach.

Q1 loadings amounted to 278 kt.

Equatorial Guinea

Punta Europe floating LNG plant (3.7 MTPA) continues stable shipments. Q1 loading amounted to 630 kt. Achieved utilization is 68%.

Cameroon

Q1 loading amounted 218 kt Cameroon floating LNG plant (2.4 MTPA).

Hilli Episeyo (7382720), which is the basis of this LNG plant, will finish its work in Cameroon in December 2026 and will be moved to Argentina for a new GLNG project.

Nigeria

Volume of loadings at Nigeria's only LNG plant in Q1 amounted to a record 4.8 million tons during the observation period. Utilization of design capacity (22.2 MTPA) - 87%. Most of the cargo went to Türkiye, India and Spain.

Mauritania and Senegal

Q1 2026 at Greater Tortue Ahmeyim FLNG loadings amounted to 688 kt. It shows that Greater Tortue Ahmeyim FLNG reached its designed 2.5 MTPA capacity. Q1 utilization amounted to 110%.

Algeria

Loadings at the country's two LNG plants amounted to 2.4 million tons in Q1 2026. Utilization of design capacity (25.5 MTPA) - 37%.

Decline in gas production and prioritization of domestic market and pipeline exports have led to low and continuing to stagnate LNG plant loadings.

Türkiye is key importer of Algerian LNG.

Details of Algerian exports are available at the link.

Regasification terminals

As of 08.04.2026, there were 206 regasification terminals in the world with a total regasification capacity of 1099 MTPA.

In 2026, it is expected that 90 MTPA of regasification capacity will be commissioned. China will continue to be the leader, with 38 MTPA of new build-up.

Discharge

According to Seala AI, Japan regained the title of the main importer of LNG in the world as result of Q1. The key reason is decline of Chinese LNG import. South Korea is the third with a slight lag behind China. India reduced LNG imports and took only the sixth place in the ranking of importers.

China

LNG infrastucture

China continues to dominate in regas capacity newbuild. China continues to rely on its gas infrastructure and actively develop it. China is flexible in LNG purchases - balancing is carried out by pipeline gas, coal, and hydroelectric power plants.

As of 08.04.2026, there are 38 operating regasification terminals in mainland China with total capacity 165 MTPA (excluding Taiwan province) and 3 terminals with total 20 MTPA in Taiwan province.

2026 is expected to be a record year for the commissioning of regasification terminals in China - 38 MTPA. Although many projects scheduled to go online this year, previosly was delayed. Probably only a portion of regasification terminals under construction will be completed de facto.

There is already some regional surplus of regas capacity. It led and keeps leading to low utilization levels for new and existing terminals.

LNG import

LNG deliveries to China totaled 14.8 million tons in Q1. Utilization of regasification terminals with 165.4 MTPA design capacity was 36%. Q-o-Q decrease is 4.8 million tons (24%). It is the lowest level since our observation started (Q4 2022). Natural gas supplies from Russia to China via Power of Siberia increased in the end of Q4. It decreased demand for LNG.

Q1 LNG imports in Taiwan province amounted 6.0 million tons. Utilization of the regas terminals (20.0 MTPA) was 120%. LNG import volumes have been relatively stable for a long time and slowly growing with overall GDP growth.

Israeli-US war against Iran led to halt of Qatari LNG supplies to China since the end of March. Namely Qatar became the leading supplier of LNG to China in 2025. China will be forced to increase its purchases of Australian LNG in Q2. There is a chance that Chinese state-owned companies will open their terminals for Russian LNG from Arctic LNG 2 and Baltic medium-tonnage projects. Similar discussions are taking place in oil market regarding admission of Russian "sanctioned" oil to crude import terminals of Chinese state-owned oil companies.

LNG re-export

In Q1, China re-exported 1.3 million tons of LNG (19 cargoes). Of these, ten shipments went to South Korea, five to Thailand, and the rest to Japan, India, and Philippines.

Details of Chinese gas market are available here.

Japan

In Q1, Japan imported 18.8 million tons. Utilization of regas capacity (216 MTPA) was 35%. Japanese regas capacity is in excess. Excess capacity created for insuring that peak seasonal and regional demands will be met, as well as overcoming possible problems with nuclear and coal generation.

Qatar and UAE aren’t major LNG suppliers in Japan. Three-quarters of LNG import are based on long-term contracts and oil-indexed formula prices. Japanese import has not suffered due to the closure of the Strait of Hormuz. However, due to mechanics of price formulas increase in oil prices will affect cost of LNG import in 2026.

Japanese government continues to successfully obtain “permits” from Trump to import Russian LNG from Sakhalin-2.

South Korea

Q1 LNG import totaled 13.2 million tons. Utilization of the design capacity of regas terminals (146 MTPA) is 36%. Qatari supplies vanished in H2 March. Qatar became the number two LNG supplier to South Korea in 2025 (7.4 million tons). It will be a challenge for KOGAS.

Singapore

LNG deliveries to Singapore in Q1 amounted to 1.3 million tons.

Details of the import and re-export of LNG by Singapore are available at the link.

Thailand

Q1 LNG imports amounted to 3.1 million tons. Utilization of the terminals (19 MTPA) was 65%.

Gas-fired TPPs account for more than half of power generation in Thailand. Therefore, LNG demand strongly depends on seasonality of electricity demand and availability of cheaper sources of electricity (primarily hydroelectric power plants).

The period from March to May is the peak period in terms of electricity demand.

India

Q1 LNG imports amounted 5.9 million tons. Utilization of terminals (51.5 MTPA) was 46%. In March, supplies of Qatari and Emirati LNG were halted, which reduced total volume of LNG imports into the country. There were almost no substitute supplies from other countries.

Qatar became the leading supplier of LNG to India in 2025 (11.8 million tons). UAE, which also are off the market, was the second leading supplier (2.9 million tons).

Heavy dependence on Qatar in LPG and LNG import lead to signigicant energy crisis in the country. This affects cooking processes of hundreds of millions of poor and low-income Indians. Energy crisis in India will deepen in Q2 due to blockade of the Strait of Hormuz and the Iranian coast by USA. India could easily import Russian LNG and LPG at any time with short notice - everything depends on Modi’s desire to execute sovereign energy policy.

On top of it will affect domestic fertilizer productions. Which in turn will lead to lower crops this and next season. In case of prolonged blockade of the Strait of Hormuz prices for locally produced food (starting with wheat) will skyrocket this autumn.

LNG itself accounts for half of India's natural gas market (the rest is locally produced gas). India's energy system is predominantly coal-based and can withstand reduced gas supplies. However, simultaneous market crisis in LNG, LPG, and oil supplies, coupled with rising energy import prices, places immense pressure on India's financial system. Rupee's exchange rate is currently being artificially maintained through burning of Indian gold and foreign currency reserves. Prolonged war in Middle East will inevitably lead to a weakening of rupee and further increases in energy import prices denominated in rupees. All of this leads to a collapse in domestic gas demand, primarily aming domestic fertilizer producers.

Pakistan

Q1 LNG imports amounted 1.2 million tons.

Qatar provided almost 100% of LNG imports to Pakistan. At the same time, Pakistan faced the problem of excess supplies due to stagantion of domestic gas market. In recent years, Pakistan has cancel a lot of Qatari LNG cargoes due to oversupply even under pre-war price levels. In March the problem became the opposite - Pakistan is forced to find all the necessary import volume on spot (!) market. As the result March 2026 discharges shrinked. This will create crisis conditions for poor Pakistani gas market.

Kuwait

Q1 discharge volume amounted to 398 kt. Utilization of the only regas terminal (11.3 MTPA) was 14%.

Traditionally, peak demand for LNG is observed in May-October due to high demand by gas TPP. In winter, demand for LNG is 2-3 cargoes per month.

In 2025, 5.3 million tons of LNG were supplied from Qatar (market share - 69%).

Iraq

After Israeli strike to South Pars Iran stopped export flow to Iraq to stabilize own gas market.

Gas supply of Iranian gas to Iraq amounted to 55 mcm/d. It is about 40% of Iraqi gas demand. its gas supply, will face an unsolvable problem of not meeting domestic demand during the upcoming heatwave. The country is expected to experience widespread power outages this summer.

In March 2026, gas production in Iraq had halved to 11.3 mcm per day.

Installed capacity of gas-fired TPPs in Iraq is 33.6 GW. Theoretical maximum demand from gas generation is 200 mcm/d. In July and August, everything which could generate electricity, will do it. Any disruption in gas supplies will lead to a limitation of power supply.. In August 2025, due to a 30 mcm/d decrease in Iranian gas supplies to Iraq, there were power outages.

Egypt

Q1 discharge amounted to 2.9 million tons. USA dominates in Egyptian LNG import - 2.3 million tons.

Gas supplies to Egypt from Israeli Leviathan platform in the amount of 28 mcm per day were halted from February 28 to April 3 due to Israeli war against Iran and preventive shutdown of production at the field.

Türkiye

Q1 discharge amounted to 6.1 million tons. Traditionally, Türkiye actively imports LNG during the cold months from November to March. USA supplied 3.7 million tons. Algeria - 0.7.

On 02.01.2026, Azerbaijan and Türkiye signed an agreement on the supply of natural gas from Absheron gas field in Azerbaijani sector of Caspian Sea with an annual volume of 2.25 bcm (6 mcm per day) starting from 2029 for 15 years via the existing Baku-Tbilisi-Erzurum pipeline.

On 09.01.2026 Australian Woodside and BOTAŞ have signed a long-term agreement to supply LNG to Turkish market. Under the contract, Woodside Energy will supply BOTAŞ approximately 500 kt annually for up to nine years, beginning in 2030. LNG will come primarily from Louisiana LNG project in USA, as well as from other Woodside assets.

In February 2026, BOTAŞ announced the construction of a second phase of a regasification terminal in Dörtyol in Hatay province. It will be based in FSRU as well. The capacity will be 7.5 million tons per year, which is equivalent to the first FSRU Ertuğrul Gazi. Additionally, BOTAŞ is considering the construction of a new terminal on the Mediterranean coast between Gazipaşa and Anamur.

Türkiye keeps it energy source diversification.

After Israeli strike to South Pars on 18.03.2026 Iranian pipeline supplies are at risk. Türkiye will be forced to increase purchases LNG on international market. Ability to import additional volumes of Russian pipe gas is limited by current high utilization rate of both Turkish stream, and Blue stream. There may be an optimization of timing of summer repair campaigns for these gas pipelines. Russia is interested in increasing its gas supplies to Turkey. However, Ukraine with assistance of UK and USA continues to attack infrastructure of Blue Stream and Turkish Stream pipelines. On March 17-19, 26 Ukrainian UAVs attacked Russkaya and Kazachya compressor stations of Blue Stream gas pipeline and Beregovaya compressor station of Turkish Stream gas pipeline. The attacks were repelled. Total capacity of the gas pipelines is 47.5 BCMA (130 mcm/d). If future attacks are successful, Turkey may face an energy crisis. Summer season is low on Turkish market. This significantly reduces impact of the current global gas crisis to Turkish market.

Details of Turkish gas market are available here.

EU and UK

Gas production

In 2026 Romania is top EU gas producer with 22 mcm of average production.

In recent years, Cyprus has discovered a number of large gas fields in its offshore economic zone - Kronos, Aphrodite, Pegasus. The total estimated reserves amount to about 566 billion cubic meters. It is planned to start exporting to the rest of the bloc through Egyptian LNG plants starting in 2027.

Planned tax on external imports of natural gas

European Commission plans to introduce another tax on the external import of resources to the EU - Methane Regulation (Regulation (EU) 2024/1787). Official wording is based on methane emissions at its production. Transportation and regasification segmets and foreign upstream projects controlled by EU companies will be excluded from the tax. De facto, this is a hidden taxation of gas supplies from the United States, Qatar, Algeria, and Azerbaijan.

In December 2025, the European Commission proposed to the LNG exporter from the United States the procedural facilitation of the “audit” of gas fields. The US Chamber of Commerce once again rejected both the procedural relief and the entire initiative, as the US government basically does not want to pay any tax on its LNG.

Gas stocks at UGS

As of 07.04.2026, remaining stocks of active natural gas in UGS of EU and UK amounted to 32.1 bcm. Stocks are significantly lower than in previous years – minus 6.7 bcm compared to previous year and minus 33.3 bcm compared to 2024. It is second lowest volume after 2022.

Heating season lasted from 17.11.2025 to 02.04.2026.

Net gas withdrawals out of UGS in Q1 2026 amounted to 34.1 bcm. It is 2.6 bcm less than in Q1 2025.

Given backwordation of gas futures market, it is unprofitable for private gas companies to buy gas now, store it, pay interest on a trade loan, and then resell it cheaper. Lack of commercial stimulus will lead to reduced volumes of LNG purchases for injection into UGS facilities - injection will be carried out only under pressure from European Commission and national authorities.

Regas terminals

As of 08.04.2026 there are 41 regasification terminals in EU and UK with total capacity 212 MTPA.

In December 2025, Zeeland Energy Terminal developed by VTTI and Höegh Evi passed FID. The terminal will be located in the Vlissingen-Oost port area of Zeeland province of the Netherlands. ZET will be a floating terminal for importing LNG with a direct connection to the country's national gas network. ZET FSRU is scheduled to be commissioned in Q3 2029.

LNG import

Q1 discharges amounted to 35.0 million tons. Utilization of regasification terminals - 66%.

The top LNG importers in Q1:

France - 5.4 million tons.

UK - 5.2.

Spain - 5.1.

Netherlands - 3.9.

Italy - 3.4.

In Q1 USA strengthened its positions in EU and UK - 20.5 million tons. Share of US import amounted to 60% (Q-o-Q growth 3%). Trump's position is to increase the US share up to 100% as new LNG projects are launched in USA and put EU and UK under full energy dependence on US energy supplies. European Commission accepted risk of complete energy dependence on USA and even started standoff with Qatar and planned complete abandonment of Russian gas import.

Russia took the second place in Q1 with 4.8 million tons. Russia's current share in EU and UK LNG market remains at 14% level. Russia supply LNG to EU only from Yamal. LNG from Baltic medium-tonnage projects and Arctic LNG-2, which are not favored by the West, is not taken at all by EU countries. Yamal LNG is traditionally taken by 4 countries - Spain, France, Belgium and Netherlands. Other EU countries are avoiding Yamal LNG even in time of gas crisis. At the same time, since December 2025, Yamal LNG has been discharges only in EU. On 03.12.2025 European Council and European Parliament decided to limit EU countries from possibility to import Russian pipeline gas and LNG. LNG supplies under current short-term contracts signed before 17.06,2025 are “allowed" until 25.04.2026.

Qatar continued to be the number three in the ranking of LNG suppliers to EU and UK with volume of 2.2 million tons and 6% share. Due to the blockade of the Strait of Hormuz there will not be Qatari LNG in EU and UK in Q2.

New supply contracts

In February 2026, German energy company RWE signed a LNG SPA with ADNOC of UAE. The contractual volume of supplies is 1 MTPA for 10 years.

Details of LNG imports by EU countries are available at the link.

Ukraine

In March, Ukraine tried to lift a long-standing Turkish restriction on transit of LNG carriers through Istanbul. Türkiye refused due to potentially huge damage in case of an explosion of loaded LNG carrier in city area. It was Ukraine that set the precedent this March for the attack on a LNG carriers.

Gas reserves at UGS as of 07.05.2026 amounts to 5.2 bcm, which is the highest in SVO era. Injection of natural gas into UGS has started on 13.03.2026. In total, Ukraine needs to have about 8-9 bcm by beginning of heating season. Unlike anti-record last year, summer gas injection program will amount to only 20 mcm per day.

All gas purchases are financed by EU and Norway in the form of direct or indirect loans and grants. Almost all injected molecules of gas are coming from Texas and Louisiana.

Brazil

Brazil's LNG regas infrastructure consists of 8 terminals with a total capacity of 36 MTPA. LNG traditionally performs reserving function and insures the country's gas-fired TPPs are well supplied by gas during periods of low domestic hydro generation. Hydroelectric power plants accounted for 56% of the country's electricity generation in 2024. 24% was generated by WPP and SPP.

Q1 LNG imports to Brazil amounted to 470 thousand tons. Terminal utilization is a meager 5%.

Argentina

Argentina has signed the first LNG SPA in a new era. The contract was signed by the Southern Energy consortium with the ex-Gazprom Germany (temporarily stolen by the German government and known during this period as SEFE). The contract provides for the supply of 2 MPTA for 8 years, starting in 2028. This is equivalent to 80% of the capacity of the first FLNG plant of the consortiun. The consortium includes Pan American Energy (40%), Pampa Energy (20%), Harbor Energy (15%), Golar (10%) and the state-owned company YPF (with tiny 15%). The LNG project's resource base is shale gas production in Vaca Muerta formation.

This is Argentina's first LNG project to materialize (apart from the Bahia Blanca floating LNG plant, which lasted about a year). Together with the planned capacities, for which final investment decisions have not yet been made, Argentina will be able to export up to 28 MTPA by 2035. This will make it a significant player in the international market.

Fleet

Current fleet

As of 07.04.2026, there are 819 operational linear LNG carriers, excluding bunkering vessels, FSRU, FLNG, FSU and combined LNG and LPG carriers, with 58.3 MT of total cargo hold capacity.

Newbuild

LNG carriers with 7.5 MT of total cargo hold capacity are expected to be commissioned in 2026. It will be all-time high value. Expected Y-o-Y increase is 21%.

South Korea is the leader in LNG shipbuilding. Japan, historic leader in the construction of gas carriers, systematically stopped their construction for internal economic reasons. South Korea has won this competition and currently dominates among existing fleet and among LNG vessel under construction.

China pursue South Korea, moving from building relatively cheap oil tankers and bulk carriers to building much more expensive LNG carriers. China is the number two shipbuilder of LNG carriers right now with a dynamically growing market share. Prospects of Chinese shipbuilding are limitless.

In Q1 new Arc7 ice-class LNG carrier Konstantin Posyet (9904704) underwent sea trials. In addition, two new LNG carriers Petr Stolypin (9904675) and Sergey Witte (9904687) are expected to be completed by Zvezda shipyard in 2026.

In March 2026, Novatek created a subsidiary Northern Engineering for construction of LNG carriers. Taking into account that Ilya Luschikov, who also heads the Murmansk LNG project, is in charge, it is likely that this new LNG gas carrier construction site will be based on dry dock of Center for construction of large-capacity offshore structures in Belokamenka, Murmansk region. In this case, this means a refocus of Novatek construction of floating LNG trains, which are not in demand under current market conditions, to construction of ice-class LNG carriers, which Novatek really needs to export LNG from Yamal and Artic 2 LNG plants.

Blockade of Strait of Hormuz

As of 08.04.2026, there are 16 linear LNG carriers blocked in Persian gulf. You could monitor in real time this part of the world LNG fleet in our live map.

Market view for Q2 2026

Primary consumption of natural gas in traditional LNG markets in Q2 is traditionally the lowest through a year. EU UGS refilling will determine LNG demand in Q2.

The “truce" between USA and Iran is unlikely to last long. In the event of a resumption of war activities, the situation on the global LNG market will return to the status quo that was observed in March 2026. Paid nature of passage of Strait of Hormuz will not have a significant impact on the global LNG market, the key thing is possibility to export Qatari and Emirati LNG from Persian gulf.

India, Pakistan, and Bangladesh are the main victims of the closure of the Strait of Hormuz. Energy crisis in India will deepen in Q2 due to blockade of the Strait of Hormuz and the Iranian coast by USA. India could easily import Russian LNG and LPG at any time with short notice - everything depends on Modi’s desire to execute sovereign energy policy.

At the same time, for economic reasons, we may see an increase in LNG trade within the gulf itself. In scenario of a prolonged halt in military operations in the gulf and the continued blockade of the Strait of Hormuz, QatarEnergy may restart some of its LNG trains to meet demand for LNG within Persian gulf. From May to September, demand for electricity and natural gas for its production peaks in Middle East. This will allow restart of several trains at the plant (up to 25% of its capacity).

Trump can add new shock to the LNG market again at any time, including new tariff , new wars (bombing Iran, seizing Greenland and other), beginning of new round of pressure on Russia or China. Absolutely any thought can come into his red head. After the war US financial system has seriously deteriorated, world LNG market is moving towards a surplus - therefore something will definitely happen. A gas summer is a convenient period for this volatility. New pressure on Yamal LNG and Sakhalin-2 is likely in 2026.

In Q2 EU will lose its second (Russia) and third (Qatar) LNG suppliers. Gas flow of Russian gas to EU via the first line of Turkish Stream could be aborted at anytime after an Ukrainian attack. EU is close to 100% dependence on US LNG supplies. USA is one step away from energy monopoly.

EU has sufficient gas stocks in UGS. Given backwordation of gas futures market, it is unprofitable for private gas companies to buy gas now, store it, pay interest on a trade loan, and then resell it cheaper. Lack of commercial stimulus will lead to reduced volumes of LNG purchases for injection into UGS facilities - injection will be carried out only under pressure from European Commission and national authorities.

Notes:

Join Seala AI’s Linkedin page to be informed for all new future releases with new dashboards and insights.

Non-mainstream oil and gas news and views are available in Seala AI’s telegram channel.

Full set of reports for each country and much more information are available via Seala AI terminal.